@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting Forecast (2026–2032): Hummus Market to Reach USD 7,553.7 Million by 2032 from 2025 Base (USD 3,736.0M) at a 10.95% CAGR — North America Leads with USD 1,894.36M in 2025

Hummus Market 2026: Strategic Imperatives from PW Consulting’s New Market Research Brief

Executive snapshot

As demand for plant-based, convenient protein options accelerates, the global hummus market has matured from a niche specialty shelf to a mainstream retail and foodservice category. PW Consulting’s latest Hummus Market research—anchored on a 2025 base year and spanning the 2026–2032 forecast horizon—reveals a sector growing at a sustained compound annual growth rate (CAGR) of 10.95%. From an estimated USD 2,308.29 Million in 2020, the market expanded to USD 3,736.0 Million by 2025 and is projected to reach approximately USD 7,553.72 Million by 2032 (USD, Million). These headline figures frame the strategic choices manufacturers, retailers, and investors must make in 2026 to capture disproportionate value.

Hummus Market

Why this brief matters for 2026 decisions

- Macro clarity: The brief translates high-level growth into operationally relevant scenarios—base, upside, and downside—so teams can size the prize for product launches, manufacturing scale-ups, and channel expansion without guessing.

- Risk-informed action: Recent supply-chain and regulatory shocks (detailed below) make 2026 a year for proactive risk mitigation rather than reactive crisis management. Our model quantifies exposure to raw-material price swings and labeling/regulatory incidents to inform hedging and inventory strategies.

- Competitive positioning: With top-three and top-five concentration ratios at 38.6% and 48.2% respectively, the category is neither a monopoly nor atomized—leaving room for leading brands, strong challengers, and disciplined private-label entrants. The study identifies structural advantages that will deliver market share gains in 2026 and beyond.

What’s contained in the report (practical, usable deliverables)

- Robust market sizing and forecast model (2020–2032) with downloadable Excel workbooks that allow scenario toggling of price, volume, and ingredient cost assumptions.

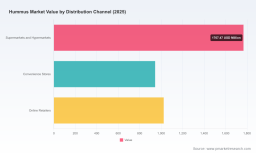

- Segmentation framework across Region, Product Type, and Distribution Channel—mapped to demand drivers and SKU economics. Note: detailed segment-level figures are reserved for the full report to protect commercial sensitivity and to encourage direct engagement.

- Channel playbooks for Retail, Convenience, and E‑commerce—covering assortment strategies, promotional cadence, and category resets that increase velocity and margin.

- Go-to-market and SKU rationalization templates that quantify when to invest in premiumization, single-serve innovation, or cost-competitive formulations.

- Supplier and ingredient risk matrix focused on chickpeas, tahini, and olive oil—plus negotiation levers for longer-term contracts, indexed purchasing, and geographic sourcing diversification.

- Regulatory incident response checklist and a recall-readiness playbook—aligned to recent FDA Class II events described below.

- Competitive benchmark dossiers on incumbent and growth players, including strategic profiles, route-to-market, innovation pipelines, and M&A signals.

- Investment memos and financial sensitivity analyses for M&A, private-label entry, and plant-capacity expansion decisions.

Market dynamics shaping 2026 strategic choices

Consumer demand continues to bifurcate along two axes: convenience and premiumization. Retail observers and company disclosures indicate rising demand for single-serve, on-the-go formats, while premium lines and chef-inspired flavors are driving higher ASPs in club and specialty channels. Packaging innovations—resealable tubs and integrated snack pots—are not peripheral; they are core to repeat purchase and trip conversion.

Hummus Market

On the supply side, hummus production is inherently exposed to agricultural volatility. Chickpeas, tahini (sesame paste), and olive oil remain the principal cost drivers. Price volatility from weather-driven yield changes and shifts in global oilseed markets can materially alter gross margins within a single harvest cycle. PW Consulting’s models allow procurement teams to stress-test margins under multiple agricultural price-path scenarios and to evaluate the business impact of forward contracts, inventory buffers, and supplier diversification.

Hummus Market

Regulatory and food-safety events have an outsized reputational and P&L impact in this category. Notable incidents over the last 18 months include a voluntary recall tied to missing refrigeration labeling in July 2025, and Class II FDA recalls related to foreign material contamination and undeclared allergens in 2025–early 2026. These events underscore the need for tighter labeling controls, supplier audits, and robust lot-traceability systems. The full report maps incident frequency to expected revenue-at-risk and prescribes operational controls calibrated to company size and distribution breadth.

Competitive landscape: what to watch in 2026

The category features a mix of large-scale branded players, regional specialists, and artisan/innovator brands. Leading multinational-backed manufacturers maintain the largest retail footprints and category-defining SKUs; mid-sized and regional producers compete on organic claims, flavor innovation, and agility; artisan brands lean into provenance and chef collaborations.

- Sabra Dipping Company, LLC (White Plains, NY): As a U.S.-based market anchor with backing from major food groups, Sabra combines scale manufacturing, retailer relationships, and portfolio breadth. Market signals indicate rising demand for single-serve packs—a lower-margin but high-velocity format that large players are well-positioned to dominate via shelf prominence and co-marketing with retailers.

- Cedar’s Mediterranean Foods, Inc. (Haverhill, MA): Cedar’s recent packaging redesign and launch of a premium Reserve line show a dual strategy: tighten operational efficiency on core SKUs while pursuing higher-margin innovation. Such moves are instructive for mid-sized producers evaluating trade-offs between SKU proliferation and pack rationalization.

- Tribe Hummus and other flavor-focused brands: These challengers expand category appeal through health-forward positioning and flavor extensions that drive incremental basket spend. Their agility in flavor testing provides a roadmap for rapid prototyping and localized launches.

- Regional and artisanal entrants (Ithaca Hummus, Hope Foods, Lantana Foods, Haliburton International): These brands exploit authenticity, regional sourcing, and co-branding (e.g., olive oil partnerships) to secure premium shelf niches and foodservice placements.

- Large multi-category suppliers (Boar’s Head, Bakkavor Group Plc): With broader deli and prepared-food portfolios, these players leverage cross-category distribution and manufacturing synergies to enter or scale within hummus effectively.

Our competitive analysis is forward-looking: we flag which capabilities—cold-chain logistics, SKU rationalization, co-man manufacturing, private-label partnerships, and e‑commerce fulfillment—will decide who scales profitably in 2026.

Strategic playbook for 2026 (high-impact actions)

- Prioritize format economics: Run SKU-level profitability for single-serve vs multipack vs resealable tubs. For many players, single-serve will be an acquisition channel; for others, it may be margin-dilutive without scale.

- Hedge ingredient exposure: Implement multi-year procurement strategies for chickpeas and sesame, combine spot exposure limits with annualized forward purchases, and evaluate alternative tahini suppliers and geographies to reduce concentration risk.

- Invest in labeling and traceability: Upgrade packaging verification processes and lot-trace systems to reduce recall frequency and severity—an investment that pays back via lower recall costs and preserved retail listings.

- Segment go-to-market by retailer economics: Apply the report’s retailer scorecards to determine which accounts justify premium SKUs, which require price-led assortments, and where e-commerce can subsidize national brand building.

- Use M&A strategically: Target acquisitions that fill capability gaps—co-man capacity, refrigerated distribution reach, or D2C capabilities—rather than purely chasing incremental volume.

Tools inside the report that accelerate execution

- Interactive scenario models to quantify P&L sensitivity to ingredient prices, promotional intensity, and channel mix shifts.

- Retailer negotiation playbooks with NRV (net revenue value) calculators and recommended promotional mechanics by channel.

- Recall-cost estimator and supplier audit templates that reduce time-to-action during incidents.

- Innovation prioritization matrix that balances margin potential, manufacturing complexity, and speed-to-market.

Final perspective

2026 will be a decisive year for market participants. The hummus category is expanding rapidly—driven by convenience-led formats and premiumization—but it is also increasingly sensitive to ingredient volatility and regulatory scrutiny. Firms that combine disciplined procurement, rigorous labeling and safety controls, and a clear SKU-to-channel strategy will capture the biggest share of the available growth embodied in a market growing at an approximate 10.95% CAGR through 2032.

PW Consulting’s Hummus Market report is built to translate that growth into boardroom-ready choices: operational investments, M&A targets, portfolio strategies, and channel tactics. For access to the full segmentation data, downloadable financial models, and the complete competitive dossiers (including quantified segment shares and unit economics), please refer to the full report on our website or contact your PW Consulting industry lead.

For detailed analysis of this topic, please visit the official page: Hummus Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com