@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting Report: Prostate Cancer Devices Market Set to Rise from USD 4,325 Million (2025) to USD 8,227 Million by 2032, Backed by a 9.85% CAGR

Prostate Cancer Devices Market: Strategic Imperatives for 2026

Executive snapshot

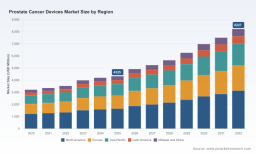

PW Consulting’s new Prostate Cancer Devices Market report reframes the next strategic inflection point for medtech leaders, payers, and private equity investors focused on urologic oncology. The market we modelled shows a robust expansion from the 2025 base year—USD 4,325 Million—to an expected USD 8,227 Million by 2032, underpinned by a compound annual growth rate (CAGR) of 9.85% over the 2026–2032 forecast window. The historical trajectory (2020–2025) already demonstrates accelerating adoption of image-guided diagnostics and minimally invasive focal therapies; the coming planning cycle will be defined by reimbursement realignment, AI-enabled care pathways, and consolidation around platform plays.

Prostate Cancer Devices Market

Why this report matters for 2026 decisions

Executives preparing capital allocations, product roadmaps, or M&A activity for 2026 need more than a top-line projection. They need a decision-grade synthesis that translates market economics into go/no‑go triggers, launch sequencing logic, and evidence-generation priorities. Our report delivers precisely that: it converts a clear market CAGR and multi-year upside into tactical options that can be executed this calendar year.

Prostate Cancer Devices Market

- Prioritize spend: identifies which technology archetypes require clinical evidence to unlock reimbursement, and which can grow on coverage momentum and hospital capital cycles.

- De‑risk launches: provides a staged market-entry playbook that ties regulatory pathways to payer engagement milestones and KOL adoption curves.

- Target M&A: combines concentration metrics and capability mapping to reveal where bolt-on acquisitions accelerate value capture versus greenfield investment.

What’s inside the report — operational, not academic

This is a practitioner’s deliverable built to be used in boardrooms, investment committees, and commercial planning sessions. Highlights include:

Prostate Cancer Devices Market

- Market sizing and scenario models calibrated to a 2025 base year and run across 2026–2032, with sensitivity analyses that quantify downside/upside under alternative reimbursement outcomes.

- Technology landscape and competitive positioning maps that cluster devices by therapeutic intent (diagnostic vs treatment), modality, and hospital capital vs consumable revenue mixes—without revealing client‑reserved subsegment numbers in this public synopsis.

- Regulatory and reimbursement playbooks: a step-by-step guide to typical 510(k)/de novo/Breakthrough Device timelines, evidence expectations, and payor-engagement cadences tailored to focal therapy, brachytherapy, cryotherapy, HIFU, and MRI/ultrasound-guided biopsy platforms.

- Commercialization toolkits: go-to-market archetypes for global rollouts, pricing and contracting templates, hospital adoption accelerants, and sample value dossiers for payers and HTA bodies.

- Investment intelligence: vendor scorecards, diligence checklists, a buy-versus-build decision matrix, and a prioritized list of capability gaps attractive to strategic acquirers.

- Actionable risk maps and mitigation plans charted against coding, reimbursement, and clinical-trial timelines for 2026–2028 decision windows.

Competitive landscape — who matters and why

The prostate devices ecosystem remains meaningfully concentrated, with the top three competitors collectively controlling a majority of installed platform revenue and the top five extending that lead modestly. That concentration creates both barrier and tailwind: incumbents control platform-level customer relationships, but emerging adjuncts and AI-enabled diagnostics create predictable entry points for focused entrants and partners.

- Intuitive Surgical (Sunnyvale, CA): The da Vinci platform is the default minimally invasive surgical backbone for radical prostatectomy. Its installed base and workflow integration make it a strategic anchor for manufacturers of adjunct devices and perioperative implants.

- AngioDynamics (Latham, NY): The NanoKnife irreversible electroporation platform has moved from niche salvage indications to broader intermediate‑risk applications, receiving mainstream recognition for tissue‑sparing ablation performance.

- EDAP TMS (Lyon, France) and SonaCare Medical (Charlotte, NC): HIFU system providers that remain central to focal ablation discussions where non-invasive therapy portfolios are prioritized.

- HealthTronics (Austin, TX), Perineologic (US), and Profound Medical (Ontario, Canada): Providers spanning cryotherapy, transperineal biopsy access, and MR/US fusion systems—each offering tactical hooks for channel partnerships and platform bundling.

- Insightec (Tirat Carmel, Israel), Francis Medical (Maple Grove, MN), and Levee Medical (Durham, NC): innovators in MRI-guided focused ultrasound, water‑vapor ablation, and urologic scaffolds respectively—these firms exemplify how targeted new modalities can force incumbents to re-evaluate coverage and OR pathway economics.

- Electra/Major radiation and implant suppliers (Elekta, Varian, Eckert & Ziegler, Boston Scientific, Olympus): players that anchor the radiotherapy and implant markets and are important partners for hybrid care pathways combining focal therapy with radiation adjuncts.

Recent developments that change the calculus for 2026

A series of regulatory, clinical, and reimbursement events between 2024 and 2026 materially change tactics for market entrants and incumbents alike:

- Coding reform: the AMA’s decision to replace the long-standing prostate biopsy CPT code with a set of bundled imaging‑guided biopsy codes (effective January 1, 2026) shifts commercial incentive structures and increases the value of imaging-integrated biopsy platforms for hospitals and ASCs.

- Regulatory momentum for AI and novel devices: the FDA granted Breakthrough Device designation to ArteraAI Prostate and cleared new imaging workflow tools like Philips’ UroNav enhancement—both developments compress adoption timelines for AI-augmented diagnostics.

- Device approvals and recognitions: recent 510(k) clearances for focal ablation devices and public recognition of function-preserving ablation systems change payer conversations; however, reimbursement for certain modalities (notably primary focused ultrasound) remains fragmented in many jurisdictions.

- Venture and growth capital activity: targeted financing rounds for scaffold and adjunct-device firms demonstrate investor willingness to fund niche innovation that plugs into incumbent surgical platforms.

Strategic implications and a 90‑day playbook for 2026

Based on our synthesis of market growth, competitive concentration, and regulatory shifts, PW Consulting recommends the following prioritized actions for organizations looking to win in the 2026 planning cycle:

- For incumbents: double down on platform stickiness by integrating diagnostic and treatment workflows (e.g., biopsy-to-focal-therapy pathways) and establish preferred-partner agreements with promising adjunct innovators. Treat coding change as an opportunity to repackage bundled offerings with predictable hospital economics.

- For challengers and startups: focus limited clinical resources on payer-relevant endpoints (durability of cancer control, function preservation, and total cost of care). Secure a defined label/use-case that aligns with the new CPT bundling to simplify reimbursement discussions.

- For private equity and corporate development teams: prioritize targets that fill capability gaps for platform owners (software, image-guidance, periprocedural implants) over standalone small hardware plays that require long capital cycles to scale.

- For hospital systems and ASCs: model total care-path economics under the new biopsy coding paradigm and create preferred-device formularies that reduce variability in perioperative outcomes and length of stay.

How to use the full PW Consulting report

This press release is a strategic preview. The complete report contains the detailed segmentation, regional forecasts, device-level revenue models, and full vendor scorecards necessary to execute the 90-day playbook and to build financial models for transaction due diligence. It also includes proprietary scenario outputs (TAM/SAM/SOM) and a suite of slide-ready charts that management teams can use in investor presentations and board memos.

If your 2026 planning hinges on accurately sizing adoption curves, prioritizing evidence generation, or structuring payer engagements for prostate devices, this report converts market-level growth—anchored by a 9.85% CAGR and a multi‑billion‑dollar opportunity by 2032—into executable choices. For access to the full dataset, methodology, and vendor-level projections, consult the PW Consulting source release.

For detailed analysis of this topic, please visit the official page: Prostate Cancer Devices Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com