@pmarketresearch

- Followers 0

- Following 0

- Updates 57

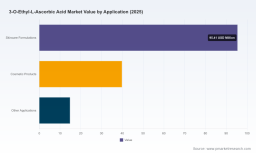

PW Consulting: 3‑O‑Ethyl‑L‑Ascorbic Acid Market to Grow at 5.8% CAGR — Rising from USD 150.0 Million in 2025 to USD 221.6 Million by 2032, Led by Asia‑Pacific (USD 51.27M)

3-O-Ethyl-L-Ascorbic Acid Market: Strategic Imperatives for 2026 — PW Consulting Market Brief

Executive summary

As senior advisors to chemical, cosmetic, and nutritional clients, PW Consulting places 3-O-Ethyl-L-Ascorbic Acid (a stabilized vitamin C derivative) at a strategic inflection point for 2026. Our latest market model — based on a 2025 base year with a historical window of 2020–2025 and a forward-looking horizon to 2032 — shows the overall market expanding at a compound annual growth rate (CAGR) of 5.8% over the forecast period. The market is estimated at approximately USD 150.0 Million in 2025 and is forecast to reach roughly USD 160.4 Million in 2026 on the path to a mid-decade target in our base scenarios. By 2032, the market size is projected to exceed USD 220 Million under our central-case assumptions.

3-O-Ethyl-L-Ascorbic Acid Market

This trajectory is underpinned by accelerating demand in formulations that prize stability and consumer-perceived efficacy, ongoing product innovation from ingredient suppliers, and a combination of capacity investments and geographic production concentration. Market concentration metrics indicate a moderately consolidated industry: our CR3 and CR5 measures suggest that a small group of suppliers exerts meaningful influence while a long tail of specialist producers remains highly relevant to customers seeking niche chemistries or tailored supply arrangements.

3-O-Ethyl-L-Ascorbic Acid Market

Why the 2026 decision window matters

-

Execution horizon for new capacity and product launches. Capacity projects, both brownfield expansions and new-build fermentation or synthesis lines, that begin permitting and commissioning in 2025–2026 determine supply balance and pricing into the early 2030s.

3-O-Ethyl-L-Ascorbic Acid Market -

Regulatory and sustainability inflection. Emerging sustainability certification requirements and new labeling guidance are moving from voluntary to contractually required for many branded buyers; firms that certify production lines early will enjoy preferential supply agreements and lower commercial friction.

-

Premiumization and formulation upgrades. Brands seeking higher-margin formats (microencapsulation, higher-purity grades, or enhanced-stability systems) will find 2026 the last clear runway to re-specify supply chains and secure long-term offtake arrangements before competition tightens.

Key strategic imperatives for 2026

-

Secure diversified raw-material and precursor supply with margin-protection clauses. The market demonstrates periodic upstream cost volatility for precursor chemicals and fermentation substrates; commercial teams should migrate to indexed pricing with cap/floor collars and dual-sourcing for critical feedstocks.

-

Pursue targeted capacity or offtake partnerships rather than broad greenfield bets. Given the mid-level concentration of suppliers, partnerships—contract manufacturing agreements, tolling arrangements, and brownfield expansions—offer better risk-adjusted returns than unrestricted greenfield investments.

-

Differentiate through formulation-enabling capabilities. Investment in high-purity grades, microencapsulation, and other delivery technologies (including recently launched microencapsulated variants) will translate into premium pricing for suppliers that can demonstrate stability, bioavailability, and extended shelf-life in real-world applications.

-

Prioritize sustainability certification across production lines. Our industry scan shows a shift toward certification of production lines under international sustainability standards. Early movers gain preferential access to multinational cosmetics and nutritional clients that increasingly require sustainability-verified inputs.

-

Embed supply-chain transparency and traceability into commercial offers. Brands are demanding verifiable chain-of-custody data and resilience guarantees; suppliers that can provide auditable traceability from precursor sourcing to finished goods will see lower buyer churn and improved contract terms.

-

Prepare M&A and bolt-on playbooks now. With about half the market influence concentrated in the top five suppliers, acquisitive players should pre-position financing and diligence templates to accelerate bilateral negotiations when opportunities arise.

Operational playbook — what to do in 2026

-

Run an immediate 90-day procurement audit to identify single-source exposures and price-index triggers. Quantify exposure to volatile precursor inputs and re-negotiate contracts where feasible.

-

Accelerate pilot partnerships for formulation upgrades — prioritize microencapsulation and stability studies that can convert shelf-life improvements into commercial premiums within 12–18 months.

-

Implement a sustainability roadmap for all production lines targeted at achieving recognized certifications within 18–36 months, aligning with major brand timetables.

-

Develop contingency logistics playbooks for alternative manufacture in India, China, and Southeast Asia CMOs; these markets already host advanced contract manufacturing capabilities and can be mobilized rapidly if supply tightness emerges.

Competitive landscape — implications for market entry and defense

The supplier ecosystem ranges from long-established chemical manufacturers in Japan and Europe to fast-scaling producers and specialist biotech firms across China and other Asian markets. Notable participants in our coverage include Shanghai Cosroma Biotech, Hubei Artec Biotechnology, Spec-Chem Industry, Bisor Corporation, Yantai Aurora Chemical, Nippon Fine Chemical, JAKA Biotech, MCBIOTEC, GfN & Selco, CORUM, Hubei Ataike Biotechnology, Lanzhou Xinweirong, Onlystar Biotechnology, KimiKa LLC (formerly Cosphatech), and Uniproma Chemical. These firms collectively represent the breadth of approaches — from high-volume industrial synthesis to niche high-purity and formulation-enabled offerings.

-

Bisor Corporation (China) recently completed a large-scale capacity expansion in Q1 2024, signaling heightened emphasis on scale as a commercial lever. Such investments can compress pricing for standard grades while creating pressure on smaller niche suppliers to differentiate.

-

MCBIOTEC (France) introduced a microencapsulated variant in mid-2024 designed to extend shelf life and ease formulation handling. This product-level innovation highlights the competitive advantage available to suppliers that pair chemistry expertise with application-focused R&D.

-

Nippon Fine Chemical and established European players continue to offer reputational advantages with long-standing quality systems and regulatory familiarity, which matter for stratified high-value contracts.

-

Multiple Chinese manufacturers and Asian CMOs provide rapid scale and cost-competitive options; however, buyers increasingly balance price against sustainability credentials and supply resilience.

Implication: new entrants and incumbent suppliers must choose between competing on scale (cost leadership) or capability (purity, delivery system, sustainability). Given observed CR3 and CR5 concentration, hybrid strategies—strategic alliances that combine European quality with Asian scale—are especially effective.

Report scope — what PW Consulting provides

Our full 3-O-Ethyl-L-Ascorbic Acid Market report is structured to support strategic decisions in 2026 and beyond. It includes:

-

A detailed historical data series (2020–2025) and a transparent forecast model spanning 2026–2032, including scenario variants (central, upside, downside) and sensitivity testing around precursor costs and adoption rates.

-

Market concentration analysis (CR3/CR5 metrics), supplier scorecards, and an annotated strategic map showing where each major supplier competes on cost, quality, and formulation enablement.

-

Supply-chain and capacity mapping, including a geo-enabled view of large-scale fermentation and synthesis facilities, outsourced manufacturing footprints, and logistics chokepoints.

-

Commercial playbooks for procurement, product development, and pricing—detailed templates to convert market intelligence into executable contract language and specification checklists.

-

Regulatory and sustainability compendium: certification pathways, likely compliance timelines, and practical steps to certify production lines under leading standards.

-

M&A and partnership pipeline: a prioritized list of target archetypes and due-diligence checklists tailored to this chemistry and its markets.

-

Primary intelligence: interviews with formulators, supply-chain managers, and C-suite decision-makers, plus tracked recent developments and a curated deal and capacity events timeline.

Dynamics and risks to monitor

-

Input cost volatility. Raw material sourcing for precursor chemicals and fermentation substrates experiences episodic volatility; firms must incorporate hedging and indexation strategies.

-

Certification headwinds. A movement toward certifying production lines under new international sustainability standards is underway; non-compliant suppliers risk exclusion from multinational formulation contracts.

-

Concentration of large-scale fermentation in China. There are significant large-scale fermentation facilities capable of annual production at scale; this structural cost advantage will influence the competitive playing field unless offset by sustainability or quality differentials.

-

Contract manufacturing diffusion. Established CMOs across India, China, and Southeast Asia have matured capabilities — an enabling factor for buyers but also a potential competitive lever for suppliers willing to outsource to flexible partners.

-

Regulatory classification and label exposure. Parts of the ingredient space overlap with nutritional supplement categories; firms must align product claims and registrations carefully to avoid regulatory friction in key markets.

How PW Consulting can help in 2026

We support clients across five engagement archetypes: rapid procurement stress-tests, formulation-to-market acceleration sprints, M&A advisory and target screening, sustainability certification roadmaps, and integrated supply-chain redesigns. Each engagement leverages the data, templates, and scenario outputs contained in the full report to convert market forecasts into executable plans within 90–180 days.

Next steps — where to access the full intelligence

This industry brief highlights the strategic options for stakeholders preparing decisions in 2026. For prescriptive subsegment-level demand profiles, granular pricing curves, supplier-specific capability matrices, and the full scenario model that underpins our USD and CAGR figures, access to the complete PW Consulting 3-O-Ethyl-L-Ascorbic Acid Market report is required. The full report is designed to be a working tool for commercial negotiations, capital allocation, and product development prioritization.

To request the complete report and our bespoke advisory services for 2026 readiness, please visit the PW Consulting research portal or contact our market team for a briefing. PW Consulting’s analysts stand ready to convert this market intelligence into a prioritized, risk-adjusted program tailored to your organization’s strategic objectives.

For detailed analysis of this topic, please visit the official page: 3-O-Ethyl-L-Ascorbic Acid Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com