@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting: Global eReader Market to Grow at 6.98% CAGR Through 2032, Fueled by Asia‑Pacific Momentum

PW Consulting: Strategic Brief — eReader Market Outlook 2026

Executive summary

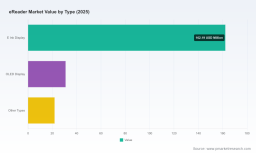

The global eReader market has entered a maturation-plus-innovation phase. Our new market study, based on a 2020–2025 historical base and a 2026–2032 forecast horizon, shows a steady expansion driven by platform convergence, component-scale effects, and renewed instructional-content adoption. The total market—measured in USD Million—grew from roughly USD 163.15 million in 2020 to about USD 215.0 million in 2025 and is forecast to approach USD 344.8 million by 2032, implying a compound annual growth rate near 7.0% (CAGR 6.98%) over the forecast window.

eReader Market

This brief synthesizes the report’s strategic implications for executive teams preparing 2026 budgets, product roadmaps, supply-chain investments, and M&A strategies. It intentionally foregrounds the analytical foundations and actionable frameworks in the full study while reserving detailed segment-level figures to the full report—designed as a gateway for decision-makers who require proprietary tables and scenario outputs.

eReader Market

Why the 2026 inflection matters

- Scale-driven cost inflection: Downstream device ASPs and module costs are being reshaped by new production capacity and JV arrangements among leading display suppliers. That dynamic creates a narrow window for OEMs to lock favorable long-term component agreements.

- Platform convergence: E-reader devices are evolving from single-purpose readers to integrated content and productivity platforms—color e-paper, Android-based ecosystems, and stylus-enabled workflows are differentiators.

- Policy and supply risk: Late-2025 and early-2026 regulatory actions targeting critical minerals and processed materials are reshaping sourcing strategies and tariff exposure. Procurement teams must incorporate new compliance and contingency layers into 2026 sourcing decisions.

What the full report delivers (practical, transaction-ready content)

The PW Consulting eReader Market Report is structured to support direct decision-making across corporate functions. Key deliverables include:

eReader Market

- Transparent market sizing and forecast model (2020–2032) with adjustable parameters for price, unit mix, and component cost trajectories—enabling scenario simulations for capex and revenue planning.

- Channel and commercial playbook: go-to-market archetypes by customer segment, subscription and content-bundling strategies, and recommended commercial KPIs for device and content revenue optimization.

- Supply-chain heatmap and supplier scorecards: component concentration analysis, lead-time sensitivity, and an actionable risk matrix with mitigations for material restrictions and tariff scenarios.

- Technology roadmap and cost curves: comparative analysis of e-paper generations, emerging color e-ink, OLED options, and the implications for battery sizing, BOM, and device form factors.

- Competitive intelligence dossiers: strategy profiles, product roadmaps, channel penetration, and three-year strategic options for the leading OEMs and ecosystem players.

- Deal origination toolkit: target screening criteria, valuation reference points, and a prioritized list of partnership plays (JV, supply agreements, content licensing) tailored to both incumbents and new entrants.

Market dynamics and strategic implications

Growth is straightforward at the top line but nuanced underneath. Our modeling shows compound growth supported by two structural trends: proliferating low-cost color and Android-capable devices that expand use cases beyond leisure reading, and stronger content-integration monetization paths (education bundles, library integrations, subscription models). Together these trends increase TAM capture potential while also creating pricing pressure in commodity hardware tiers.

From a risk perspective, the geopolitical and regulatory backdrop in late 2025 and early 2026 represents a material operational variable. Executive orders and investigations into critical-mineral supply chains, coupled with new tariff levers, create near-term input-cost volatility; procurement and product teams must be prepared with dual-sourcing and inventory strategies. Concurrently, recent capacity investments by major display manufacturers introduce future supply abundance—an opportunity for OEMs that secure early off-take terms.

Competitive landscape — positioning and strategic moves

The market remains structurally fragmented: leading consumer-platform incumbents coexist with a diverse set of specialized device manufacturers and niche ecosystem players. That fragmentation creates attractive niches for differentiated propositions and targeted partnerships.

- Amazon — Continues to leverage Kindle brand equity, integrated content storefront, and iterative hardware improvements (enhanced e-paper, AI reading-assist features). Strategic priority: defend platform lock-in via content exclusives, device subsidies, and value-added software services.

- Rakuten Kobo — Competes on openness (EPUB support) and library integrations. Strategic priority: deepen institutional channels (libraries, education) and expand multi-device content portability.

- Barnes & Noble — Pursuing hardware differentiation with ad-free experiences and partnerships (example: consumer tablet collaborations). Strategic priority: convert retail footprint and brand trust into bundled offerings and hybrid retail‑digital services.

- Onyx International — Focused on Android-based devices and color e-paper innovation. Strategic priority: push into productivity-driven subsegments (note-taking, hybrid tablet-readers) and pursue OEM partnerships abroad.

- PocketBook, ReMarkable, Bigme, Ectaco — Represent specialized approaches: premium design, e-note focus, open Android stacks, and geographically targeted portfolios. Strategic priority across these players: capitalize on product differentiation and localized distribution to avoid commoditization.

Recent product launches in 2026 underscore these strategic choices—new compact models and reading tablets signal vendors are balancing cost, battery life, and content access. For incumbents and new entrants alike, timing product introductions with supply agreements and software readiness is essential to maximize launch ROI.

Supply chain and regulatory action — what to do now

- Immediate: Conduct a three‑month sourcing stress test that models tariff shocks and single‑supplier failures. Prioritize dual-sourcing for display modules and critical ICs.

- Near‑term: Negotiate conditional off-take contracts with display manufacturers who are scaling e-paper capacity—seek clauses that align price reductions with volume milestones.

- Medium-term: Reconfigure inventory policy to balance working capital against lead-time exposure. Implement a tiered stocking approach for strategic components tied to product cadence.

Product and monetization playbook for 2026

Successful entrants will combine hardware differentiation with recurring revenue channels. Practical moves include:

- Bundled content and services: shift non‑hardware revenue to subscription and educational content packages with better lifetime-value economics.

- Modular product lines: offer a base reader with optional upgrades (color module, stylus kit, expanded connectivity) to segment pricing without proliferating SKUs.

- Enterprise and education sales: partner with publishers and institutions for bulk distribution models and long-term contracts—these channels benefit from device management and content licensing synergies.

Strategic M&A and partnership themes

Given the market’s fragmentation and the capital intensity of display production, we identify three high-probability value-creation plays:

- Strategic verticals: upstream alliances or minority investments in module suppliers to stabilize BOM costs and secure lead times.

- Horizontal consolidation: bolt-on acquisitions to fill portfolio gaps (e.g., color e-paper capability, note-taking software, or regional distribution networks).

- Platform partnerships: revenue-share agreements with publishers, libraries, and education platforms to accelerate content monetization.

What’s in the full PW Consulting report (and why you need it)

The full report contains the empirical deliverables you will reference in board meetings and investment memos: the full quantitative model (historic series and scenario-enabled forecasts), supplier and OEM scorecards, channel revenue curves, pricing matrices, product BOM benchmarking, and a prioritized list of strategic initiatives tailored by corporate profile (incumbent platform leader, OEM challenger, or new entrant). It also includes verbatim interview excerpts from suppliers, publishers, and procurement leads that informed our risk assessments.

We deliberately preserve core segmentation tables and granular regional/application splits for report subscribers. That content includes the detailed disaggregation and sensitivity runs that support capital allocation decisions—exactly the line-item intelligence CFOs and strategy teams request in diligence.

How to use this brief in 90 days

- Week 1–2: Share the report’s executive model with finance and product leaders; stress-test next year’s ASPs and BOM assumptions.

- Week 3–6: Lock in procurement options with key display suppliers informed by the supply‑chain heatmap; commence dual‑sourcing negotiations where exposure is highest.

- Month 3: Finalize 2026 launch calendar tied to component commitments, and scope any bolt-on M&A or partnerships identified in the report’s deal toolkit.

Closing perspective

For 2026, the eReader market presents an intersection of predictable growth and tactical complexity. The headline numbers—steady historical expansion, a mid-single-digit CAGR through 2032, and a meaningful upside to monetization from services—are clear. The strategic challenge for market participants is converting scale benefits while managing supply‑chain and regulatory volatility. PW Consulting’s eReader Market Report is designed to be the operational blueprint for that conversion: rigorous, scenario-enabled, and focused on executable outcomes.

To access the full datasets, segmentation tables, and the deal‑ready playbook, request the complete report and the model from the PW Consulting publications portal.

For detailed analysis of this topic, please visit the official page: eReader Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com