@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting: High‑Frequency Induction Heating Machine Market Set to Reach USD 334.11 Million by 2032, Driving a 6.5% CAGR (2026–2032)

High Frequency Induction Heating Machine Market: Strategic Imperatives for 2026 — PW Consulting Preview

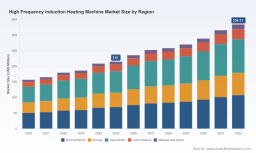

PW Consulting’s new market study on High Frequency Induction Heating Machines offers a focused strategic lens for executives preparing budgets, capex plans, and go-to-market plays in 2026. The global market has demonstrated steady expansion in recent years — rising from approximately USD 156.9 Million in 2020 to USD 215.0 Million in 2025 — and is projected to continue on a disciplined growth trajectory, reaching an estimated USD 334.1 Million by 2032. Our forecast model for the 2026–2032 horizon embeds a compound annual growth rate (CAGR) of 6.5%, and is designed to translate that macro momentum into actionable choices for manufacturers, OEMs, systems integrators, and large end-users.

High Frequency Induction Heating Machine Market

Why this report matters for 2026 decision-makers

-

Timing capital allocation: Manufacturers face competing priorities for automation, energy efficiency upgrades, and replacement cycles. The market’s mid-single-digit CAGR signals sustainable demand, but not runaway expansion — meaning investment timing and portfolio prioritization will determine winners in 2026.

High Frequency Induction Heating Machine Market -

Vendor and technology selection: Induction heating technologies span a wide power and frequency spectrum, and suppliers differ sharply on their capabilities (from compact, portable units to megawatt-class industrial systems). Our analysis maps these technological distinctions to use-case economics and operating profiles to shorten procurement cycles.

High Frequency Induction Heating Machine Market -

Risk-adjusted supply planning: Raw material and regulatory shifts are reframing the upstream economics of metal processing. Strategic sourcing decisions made in 2026 must account for material-price variability and evolving recycling mandates.

What the PW Consulting report delivers (practical contents)

-

Market sizing and robust forecasting: A top-down and bottom-up market model anchored to our 2025 base year, showing historical trajectory (2020–2025) and forward projections (2026–2032) in USD Million. The model supports scenario stress-testing against price shocks and demand-side variability.

-

Segmentation framework and buyer persona maps: Multi-dimensional segmentation (product type, application clusters, and regional demand nodes) combined with buyer personas to guide tailored value propositions — from engineering teams specifying heat-treatment cells to operations managers managing throughput and energy spend.

-

Competitive landscape & capability profiles: Comparative dossiers on incumbent and emergent suppliers, technology differentiators, service models, and distribution footprints to accelerate RFP shortlisting and supplier due diligence.

-

Commercial playbook: Procurement checklists, TCO templates, and capital-budget templates that translate product specifications into 3–5 year impact on OPEX and throughput.

-

Supply-chain and regulatory heatmaps: Identification of key supply risks and regulatory inflection points — enabling procurement and compliance teams to build mitigations and contingency plans.

-

M&A and partnership opportunity scanner: Target criteria and valuation heuristics for acquirers and private equity evaluating consolidation plays in a market with moderate top-tier concentration.

Market dynamics to watch in 2026

-

Measured growth with pockets of intensity: The overall market expansion (CAGR 6.5% in our forecast period) masks heterogeneity by application and end-use intensity. Some industrial segments are accelerating investment in induction solutions to meet throughput and precision targets; others are taking a more conservative stance tied to capital cycle timing.

-

Material and recycling policy impacts: Recent industry intelligence highlights two influences that will affect procurement and lifecycle economics in 2026. First, raw material reports show price volatility across key metallic commodities — a variable that directly alters melting and thermal-processing economics. Second, regulatory initiatives in major economic blocs are tightening the rules around scrap management and recycling flows. These policy moves change feedstock availability and create new incentives for induction-based recycling and remelting solutions.

-

Service and software as differentiation: With hardware specifications converging, aftersales service, predictive maintenance, and process-control software are emerging as key margins and retention drivers. Buyers increasingly favor suppliers that bundle field services, remote diagnostics, and integration capabilities.

-

Concentration and competitive implications: The industry shows moderate concentration at the top — the leading vendors collectively hold a meaningful share of accessible demand. For new entrants or investors, this implies the need for focused niches, service differentiation, or strategic partnerships to overcome scale disadvantages.

Competitive landscape — what we analyzed

Our vendor assessment covers a cross-section of systems providers and power-supply specialists whose products and channel strategies shape procurement choices in 2026.

-

Taylor Winfield (Warren, Ohio, USA) — A broad portfolio that ranges from kilowatt-class power supplies to multi-megawatt systems, with frequency capabilities that address a wide set of thermal-processing needs. Their breadth suits large OEM and integrator partnerships.

-

Ambrell (Rochester, New York, USA) — Known for precision systems and global installations; recent trade-show visibility underscores continued focus on technology showcase and customer engagement in manufacturing markets.

-

UltraFlex Power (Rochester, New York, USA) — Plays to flexible power architectures and mid-to-high power ranges, with product variants that appeal to both shop-floor and industrial-scale deployments.

-

Inductoheat (Troy, Michigan, USA) — A turnkey systems and automation-capable supplier serving complex industrial accounts; competitive where integration and full-process delivery are required.

-

GH Induction (Germany) and Himmelwerk (Germany) — European engineering strengths focused on automotive, aerospace, and energy sectors, emphasizing precision, reliability, and compliance with regional standards.

-

FOCO Induction and Canroon (China) — Provide cost-competitive hardware and are active in portable and industrial segments; attractive for price-sensitive retrofit projects and emerging-market deployments.

-

Radyne (UK), EFD Induction (France), Ajax Tocco (Michigan, USA), Denki Kogyo (Japan) — Complementary regional players with specialized applications strengths, local support, and niche product portfolios.

We also track corporate activity and go-to-market signals. For example, several suppliers have increased trade-show participation and demonstrated product roadmaps in late 2025 and 2026 — an indicator that suppliers are positioning for replacement cycles and OEM-spec wins in 2026.

Strategic recommendations for 2026

-

Adopt a segmented procurement strategy: Match vendor selection to use-case economics — prioritize turnkey suppliers for complex automation needs and modular, high-frequency suppliers for targeted repairs and upgrades.

-

Lock in critical service-level agreements: Given the importance of uptime and process repeatability, secure extended service contracts and remote-monitoring provisions when negotiating purchases.

-

Stress-test capital plans for material-policy scenarios: Integrate regulatory scenario runs into 2026 capex planning to anticipate changes in feedstock availability and compliance costs.

-

Explore partnerships to offset scale gaps: For smaller suppliers or new entrants, partner with system integrators or software firms to offer bundled solutions that emulate incumbent value propositions.

-

Prioritize energy and process efficiency gains: With operating margins compressed in many metal-processing industries, favor solutions that demonstrably lower energy per part and shorten cycle times.

How PW Consulting’s deliverables support execution

Beyond headline forecasts, the report is a playbook: procurement-ready vendor shortlists, bid-evaluation matrices, capex/opex calculators, and a regulatory watch tailored to induction heating. These assets are engineered to cut evaluation time and improve budget accuracy for 2026 deployments.

Our market-concentration metrics and supplier capability maps synthesize public disclosures, device specifications, and field interviews to reveal where incumbents defend share and where disruption opportunities exist. For teams considering M&A or strategic alliances, our opportunity scanner provides valuation heuristics and integration risk flags calibrated to the industry’s current scale and concentration dynamics.

Next steps — where to get the full intelligence

This preview outlines PW Consulting’s strategic view for 2026; it intentionally omits granular segment-level tables, regional stacks, and proprietary unit-sales estimates to preserve the report’s role as the essential primary source. Clients and subscribers can access the full dataset, interactive models, and supplier playbooks through our report page, which also includes downloadable RFP templates and a buyer’s guide tailored to high frequency induction systems.

For procurement leaders, plant managers, and strategic investors preparing for 2026, the PW Consulting High Frequency Induction Heating Machine Market study turns macro growth projections (USD-based market sizing and a 6.5% forecast CAGR) into executable plans. To unlock the full datasets, vendor scorecards, and scenario models that underpin the recommendations above, visit our report portal or contact PW Consulting’s industry team for a briefing.

For detailed analysis of this topic, please visit the official page: High Frequency Induction Heating Machine Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com