@pmarketresearch

- Followers 0

- Following 0

- Updates 57

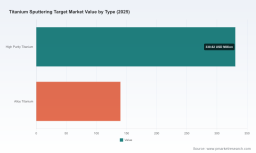

PW Consulting: Titanium Sputtering Target Market to Expand from USD 470.55 Million in 2025 to USD 794.5 Million by 2032 at a 7.8% CAGR

Titanium Sputtering Target Market — Strategic Imperatives for 2026 Decisions

PW Consulting’s new Titanium Sputtering Target Market study (base year 2025; historical 2020–2025; forecast 2026–2032) translates complex technical supply-chain dynamics into a pragmatic playbook for corporate leaders, procurement chiefs, and M&A teams preparing strategy in 2026. Built on a rigorous mix of bottom-up revenue modeling, primary supplier interviews and granular cost-driver mapping, the report synthesizes market sizing, competitive positioning and scenario-ready recommendations while preserving proprietary segmentation detail for subscribers.

Titanium Sputtering Target Market

Headline market view: scale, growth and where 2026 fits in

The market has expanded substantively during the last half decade — growing from under USD 300 million in 2020 to an estimated USD 470.6 million in 2025. PW Consulting’s forecast projects continuation of that trajectory, with the market approaching the high hundreds of millions by 2032. The modeled compound annual growth rate through the forecast window is 7.8%, a pace that signals sustained demand across thin-film, semiconductor and renewable-energy end markets. For executives, that combination of size and mid-single-digit-plus growth creates both volume-driven opportunities (scale-up, long-term contracts) and margin-management challenges (input-cost swings and spot-market exposure).

Titanium Sputtering Target Market

Why 2026 is a pivotal year for strategic action

- Demand inflection points: Semiconductor wafer processing cycles and solar-cell equipment upgrades are entering phases where sputtering-target specifications and supply consistency matter materially to OEM uptime and yield. Buyers who lock in validated suppliers early in the cycle secure technical and commercial advantages.

- Input-cost and sourcing volatility: Recent trends show upward pressure on duty-paid imported scrap values versus 2024 averages, and titanium sponge imports have seen measurable value increases year-on-year. North American titanium pricing movements during early 2026 illustrate the short-term volatility procurement teams must manage.

- Policy and trade dynamics: Import value rises and regulatory attention to sponge and scrap flows mean trade policy and customs dynamics are active risk vectors. Firms reliant on global sourcing must incorporate customs-cost and tariff sensitivity into capital planning and supplier selection.

- Market structure: The competitive landscape remains relatively fragmented — the top three and top five firms together control a minority share of the market — creating room for partnerships, regional champions, and consolidation plays.

What PW Consulting’s report delivers — practical, board-ready content

- Robust market sizing and forecast model (2026–2032) with scenario variants to stress-test demand, price and supply shocks.

- Supply-chain heat maps that identify pinch-points for titanium feedstock, fabrication capacity and critical services such as bonding and reclamation.

- Cost-driver decomposition for primary product tiers (high-purity vs. alloyed targets) to quantify margin exposure under alternative raw-material price paths.

- Competitive intelligence dossiers on leading suppliers, including technology competencies, production footprints and service capabilities.

- Actionable procurement playbooks: contracting templates, hedging approaches, and recommended inventory buffers tailored to capital-intensive buyers (semiconductor fabs, PVD tool manufacturers).

- M&A and partnership frameworks that prioritize value capture levers — access to capacity, proprietary powder metallurgy processes, and downstream reclamation streams.

- Regulatory and geopolitical scenario analysis with triggers, indicators and contingency steps for executives to embed into 2026 planning cycles.

Competitive landscape — who matters and why

Our competitive review highlights seven firms that shape technology trajectories and supply assurance in the titanium sputtering target domain. Each presents distinct strategic implications for buyers and potential partners:

Titanium Sputtering Target Market

- Materion Corporation (Mayfield Heights, Ohio) — Broad portfolio across specialty and electronic sputtering targets. Strength: deep product breadth for thin-film deposition across semiconductors, aerospace and automotive applications. Strategic implication: a go-to for integrated, cross-industry supply and rapid qualification.

- Kurt J. Lesker Company (Jefferson Hills, Pennsylvania) — High-purity titanium targets with integrated bonding and reclamation services. Strength: service-oriented model that reduces total cost of ownership for customers who need end-to-end target lifecycle management.

- Plansee SE (Reutte, Austria) — Advanced powder-metallurgy capabilities enabling high-performance rotary and planar targets. Strength: materials engineering and process control for demanding PVD coatings; attractive partner for customers prioritizing performance over commodity pricing.

- Tosoh Corporation (Tokyo) — Specialist in high-purity planar and rotary targets for semiconductor and display manufacturing. Strength: reliability in semiconductor-grade supply chains, with regional manufacturing proximity for Asia-based OEMs.

- JX Nippon Mining & Metals Corporation (Tokyo) — High-volume production capability for high-purity targets. Strength: scale in feedstock-to-target conversion; potential strategic supplier for large OEMs seeking volume certainty.

- ULVAC, Inc. (Chigasaki) — Ultra-high-purity targets focused on interconnect and barrier layer applications. Strength: alignment with advanced-node semiconductor processes that have tight contamination tolerances.

- Mitsui Mining & Smelting Co., Ltd. (Tokyo) — Comprehensive PVD target offerings for solar, display and electronics. Strength: broad product range and downstream channel presence in thin-film solar and display value chains.

Collectively these firms drive technology differentiation and service models in the market. However, market-concentration metrics show that even the largest players do not dominate — the top-three and top-five shares capture only a minority slice of total revenue — which implies opportunity for regional suppliers, specialized niche players, and third-party service providers to win tailored contracts.

Key strategic plays for 2026 — recommended actions

- Secure multi-year validated supply agreements with staged pricing floors and caps. Prioritize supplier qualifications that include bonding/reclamation capabilities to lower lifecycle costs.

- Pursue selective vertical integration or strategic equity stakes where suppliers control key powder-metallurgy processes or have reclamation networks — this is particularly relevant for firms facing tight yield tolerance windows.

- Deploy active price-risk management: combine short-term hedges with indexed contract clauses tied to transparent titanium pricing benchmarks and customs valuations.

- Invest in qualification pipelines for alternative target alloys and deposition processes. Early qualification reduces switching risk and creates negotiation leverage during demand surges.

- Evaluate M&A targets not simply on capacity, but on technology differentiation (rotary vs planar, high-purity vs alloy), intellectual property and service footprint (bonding, machining, reclamation).

- Operationalize regional redundancy: diversify fabrication footprints and logistics to mitigate Customs and trade-policy shocks that surfaced in recent years.

Risk scenarios and monitoring framework

Our scenario matrix models three primary shock pathways and the company responses that materially affect economics through 2026:

- Cost shock (raw-material spike): Rapid increases in titanium scrap and sponge costs — whether due to trade, supply reduction or surging demand — compress margins unless offset through pass-through contracts or reclamation gains.

- Policy shock (import/regulatory constraints): Tightening customs regimes or sudden tariff adjustments elevate landed costs and lengthen lead times, making near-shore capacity and qualified secondary suppliers strategic insurance.

- Demand shock (end-market downturn): Semiconductor capital-cycle shifts or solar subsidy changes can produce near-term demand contractions; firms with flexible production and blended product portfolios weather such cycles better.

For each pathway the report provides leading indicators, quantified P&L sensitivity, and a tiered response plan spanning procurement, operations and corporate development.

How PMs, procurement heads and boards should use this report in 2026

- Procurement: Adopt the report’s supplier scorecards and contracting templates as part of Q2 supplier negotiations. Use the cost-driver model to validate proposed price increases from suppliers.

- Product & R&D: Prioritize qualification efforts on target chemistries and form factors that the report identifies as growth-exposed — align R&D milestones with supplier roadmaps to reduce qualification lag.

- M&A & Strategy: Use the M&A playbook to screen targets quickly by strategic fit (technology, service, regional reach) and to size likely synergies from capacity consolidation or vertical capture.

- Board & Risk: Incorporate the report’s scenario triggers into the enterprise risk register and adjust capital-allocation stress tests accordingly.

Closing — why this report is a must-read for 2026 planners

In markets where technical performance, contamination control and supply continuity determine commercial outcomes, high‑quality market intelligence is a strategic asset. PW Consulting’s Titanium Sputtering Target Market study pairs empirical market sizing (2020–2025 historical; 2026–2032 forecast with a 7.8% CAGR) with operationally focused recommendations and competitor dossiers that translate directly into procurement strategies, R&D roadmaps and M&A screens. The report is purposely presented as a “trailer”: we provide the framework, scenarios and executive actions to move quickly, while proprietary segmentation, supplier-level pricing models and interactive dashboards are available on the report portal for subscribers and clients seeking the underlying data to execute 2026 decisions with confidence.

Download the full report or contact PW Consulting’s Titanium practice to request the subscriber-only data packs, supplier scorecards, and scenario-model templates necessary to operationalize these insights.

For detailed analysis of this topic, please visit the official page: Titanium Sputtering Target Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com