@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting: Industrial EDI Ultrapure Water System Market Set to Expand at a 5.4% CAGR

PW Consulting Releases Strategic Brief: Industrial EDI Ultrapure Water System Market — Preparing Enterprises for 2026

Executive summary

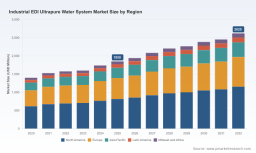

PW Consulting’s latest Industrial EDI Ultrapure Water System Market study (base year 2025) offers senior executives a decision-ready synthesis of a market that is moving from reliability-driven replacement cycles toward a multi-dimensional strategy inflection in 2026. The market reached a global size of USD 1,850 Million in 2025 and, under our core scenario, is projected to grow at a compound annual growth rate (CAGR) of 5.4% across the 2026–2032 forecast window, arriving at a materially larger market by 2032. This growth is being propelled by converging drivers: tightening regulatory ceilings on trace contaminants, electrification and semiconductor capacity expansions, and a shift to chemical-free polishing and lower life-cycle environmental impact for industrial water streams.

Industrial EDI Ultrapure Water System Market

Why this matters for 2026 corporate decisions

-

Regulatory timing creates investment urgency: Recent regulatory updates in major jurisdictions have materially tightened limits on trace contaminants, forcing operators and suppliers to accelerate adoption of chemical-free, membrane-driven polishing solutions. Procurement, environmental, and process engineering teams must reconcile compliance deadlines with capital and operational planning now — not next year.

Industrial EDI Ultrapure Water System Market -

Supply-chain and raw-material risk are front-and-center: Price and lead-time volatility for membrane-grade resins and critical components means procurement strategies, local buffer capacities, and dual-sourcing become operational imperatives to avoid project delays and margin erosion.

Industrial EDI Ultrapure Water System Market -

Aftermarket economics are reshaping supplier selection: The move to EDI-centric configurations (often paired with upstream RO stages) increases the value of comprehensive aftermarket service, remote monitoring, and consumables supply. Winning suppliers are those that can convert installed-base footprints into recurring-revenue service relationships.

Market dynamics that will shape 2026 strategies

-

Regulatory tightening accelerates adoption curves. With drinking water and discharge standards in multiple jurisdictions lowered sharply for persistent contaminants, industrial dischargers are re-evaluating chemical-intensive polishing steps. This regulatory pressure is increasing demand for technically mature, chemical-free ion-exchange and EDI solutions that can meet ultra-low thresholds while reducing hazardous waste streams.

-

Technology modularity and skid-based systems reduce deployment friction. Systems that integrate upstream RO with modular EDI stacks are enabling faster ramp-up in high-purity applications such as microelectronics and advanced pharmaceuticals. New EDI module designs now explicitly target charged-variant contaminants, providing a near-term performance uplift without wholesale process redesign.

-

Upstream capacity and materials constraints are a gating factor. Enforcement actions and production curbs on certain fluoropolymers and PFAS-related chemistries have extended lead times for membrane-grade resins and specialty polymers. Companies planning expansions or retrofit programs must bake longer procurement horizons into their schedules and consider strategic inventory or alternate-material pathways.

-

Consolidation and concentration favor scale-enabled suppliers. Market concentration metrics indicate a market where a handful of suppliers capture the majority of commercial value — a dynamic that favors players with global service networks, deep process expertise, and the ability to bundle equipment with long-term service contracts.

Competitive landscape — who to watch and what they offer

Our report provides a calibrated assessment of incumbent and challenger strategies across product, service, and go-to-market dimensions. Leading platform providers combine modular EDI stacks with upstream RO integration; others differentiate on aftermarket services, digital monitoring, and regional delivery capability. Highlights from our competitive review:

-

Evoqua Water Technologies: A proven supplier of integrated RO+EDI configurations, Evoqua’s turnkey approach — including project delivery for high-spec fabs and pharmaceutical plants — makes it a default partner for blue-chip capital projects.

-

Xylem: With targeted capacity investments to expand EDI stack output, Xylem is positioning itself to meet surging demand from semiconductor and emerging hydrogen-electrolyzer water supply projects. Their recent committed expansion underscores the importance of manufacturing scale in a constrained input market.

-

Veolia and Dow: Both leverage global systems engineering and membrane chemistry expertise to offer configurable solutions for the microelectronics and pharma sectors; their strength lies in application-specific integration and lifecycle services.

-

Regional and specialized players (Kurita, Hitachi, Pentair, Mar‑Cor, Nalco): These firms are important for customers seeking regional support footprints, localized engineering or niche product formats. Their product and service models often emphasize retrofitability and compliance-focused performance upgrades.

Recent developments that change the playbook

-

Major capacity commitments: Strategic capacity investments by established suppliers are recalibrating supply availability for EDI modules. This affects lead times and supplier negotiation leverage for large-scale projects entering procurement in 2026–2027.

-

Large-scale wins in critical sectors: High-profile turnkey contracts for wafer fabrication sites and multi-site pharmaceutical rollouts are accelerating supplier learning curves in rapid deployment, integrated commissioning, and multi-year service contracts.

-

Regulatory acceleration regarding PFAS and related chemistries: Fresh limits in key markets are prompting end-users to prioritize chemical-free polishing, which in turn favors EDI- and membrane-centric solutions while reducing long-term environmental liabilities associated with resin waste.

What PW Consulting’s report delivers (operational and strategic tools)

The report is designed as an executable toolkit for 2026 decision cycles. Key deliverables include:

-

Multi-scenario market forecasts and timing maps that align capital planning horizons with regulatory milestones and supplier capacity ramp schedules.

-

Supplier scorecards and procurement playbooks that synthesize technical performance, aftermarket economics, regional delivery capability, and regulatory compliance assurance.

-

Lifecycle TCO models for alternative architectures (integrated RO+EDI vs. standalone polishing, retrofit vs. greenfield), calibrated to real-world input-cost shocks and service-cost sensitivities.

-

Implementation risk matrices and mitigation roadmaps covering supply-chain bottlenecks (membrane-grade resins, skids, instrumentation), commissioning timelines, and operational continuity plans.

-

Actionable M&A and partnership screening criteria: target profiles, valuation levers, and integration risk checklists for companies seeking to acquire capabilities or secure supply through equity or offtake arrangements.

-

Regulatory compliance templates and internal audit checklists to demonstrate near-term adherence to emerging trace-contaminant limits while optimizing capital expenditure phasing.

How to use these insights in 2026 planning

-

Procurement teams: Recast RFx schedules to incorporate extended lead times and phased delivery options. Use competitive scorecards to weigh upfront price versus long-term service value.

-

Engineering and operations: Prioritize modular, skid-based EDI + RO solutions where rapid scale-up is needed. Run TCO scenarios that treat consumables and service as operating expenses rather than contingencies.

-

Corporate strategy and M&A: Identify targets that can immediately expand aftermarket footprints or provide raw-material hedging advantages. Factor in the strategic value of installed bases and recurring service revenue.

-

Regulatory and EHS leadership: Move from compliance-as-checklist to compliance-as-asset by quantifying avoided liabilities and waste-handling costs when choosing chemical-free systems.

Trailer note — what we are intentionally withholding here

To maintain the integrity of our publication and to encourage direct engagement with the full analysis, this press release intentionally omits granular sub-segment allocations, detailed regional split tables, and individual product price curves. The full PW Consulting report contains the complete datasets, segmented forecasts, and confidential supplier benchmarking models required to operationalize the high-level recommendations outlined above. Accessing the full dataset will enable scenario-specific quantification tailored to plant-level decisions, CAPEX schedules, and service-contract negotiations.

Final recommendation

2026 is a pivot year for industrial ultrapure water strategies: regulatory velocity, supplier capacity shifts, and aftermarket economics are converging to reorder competitive advantage across industry players. Companies that align procurement cadence, engineering standards, and service economics to these structural shifts will protect margins and capture growth. PW Consulting’s Industrial EDI Ultrapure Water System Market report provides the market sizing, risk-mapped scenarios, and transaction-grade playbooks that C-suite and business-unit leaders need to convert 2026 uncertainty into strategic advantage.

For organizations evaluating capital projects, negotiating multi-year service agreements, or assessing strategic acquisitions in the ultrapure water space, the full report is the recommended next step. Contact PW Consulting to obtain the full analysis and data toolkit to support your 2026 decision roadmap.

For detailed analysis of this topic, please visit the official page: Industrial EDI Ultrapure Water System Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com