@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting: Off-road Engines Market Poised for Recovery — Forecast to Grow at a 5.5% CAGR from 2026–2032

Off-road Engines Market 2026: Strategic Intelligence Briefing from PW Consulting

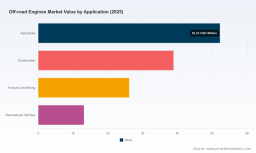

PW Consulting’s latest Off-road Engines Market report (base year 2025, historical coverage 2020–2025, forecast 2026–2032) delivers the forward-looking intelligence executives need to orient capital, product and policy decisions in 2026. Built on a blend of primary interviews, OEM and supplier financials, proprietary shipment models and regulatory scenario mapping, the study shows the market expanding at a compound annual growth rate (CAGR) of 5.5% through the forecast window. To illustrate the trajectory in plain terms: the market expands from roughly USD 130.4 Million in 2025 to an expected USD 190.6 Million by 2032 under our central forecast. This briefing highlights the strategic takeaways that should inform boardroom debates this year — and explains why the full report is an essential read for decision makers seeking actionable advantage.

Off-road Engines Market

Why this report matters for 2026 decisions

2026 is a pivot year for off-road powertrains. Regulatory tightening, multi-modal electrification, and a concentrated supplier landscape are converging to reshape risk and opportunity across OEMs, Tier-1 suppliers, rental fleets and private equity investors. The PW Consulting report translates these macro forces into practical, prioritized actions: where to direct R&D spend, which product lines to accelerate or sunset, how to approach M&A and joint ventures, and what compliance investments will materially alter total cost of ownership (TCO).

Off-road Engines Market

Data-driven foundation: what the numbers tell us

-

Historical momentum: The market demonstrated steady recovery and expansion from 2020 through 2025, driven by replacement cycles, infrastructure and agricultural equipment demand, and early adoption of hybridization in niche segments.

Off-road Engines Market -

Forward growth profile: At a 5.5% CAGR across 2026–2032, our central scenario anticipates durable growth but with increasing bifurcation between legacy internal combustion platforms and next-generation low-emission power systems.

-

Concentration dynamics: Market concentration is meaningful — the top three players account for a substantial share of global revenues, with the top five representing an even higher portion. This concentration creates both supplier leverage and consolidation opportunities for strategic acquirers.

Forces shaping the market in 2026

-

Regulation escalates the cost of non-compliance. Recent developments — notably draft Tier 5 proposals that target very deep NOx and particulate reductions and revised certification guidance for small engines — are already altering product roadmaps. Our regulatory-impact modules quantify compliance timing, retrofit economics, and potential technology mixes under alternative policy phasing.

-

Technology divergence increases strategic complexity. Electrification and hybridization are moving from demonstration to scaled deployment in specific applications, while advanced diesel and alternate-fuel solutions remain the operational workhorse in heavy-duty contexts. PW Consulting’s technology-pathway matrices map maturity, installed-cost curves, and break-even thresholds across typical duty cycles.

-

Customer economics and service models are shifting. Owners are evaluating lifecycle costs — fuel, maintenance, downtime and regulatory risk — more aggressively, creating demand for powertrain-as-a-service, sensor-driven predictive maintenance and integrated telematics packages.

-

Supply-chain fragility persists. Critical components—aftertreatment modules, high-spec machined parts and power electronics—remain chokepoints. The report identifies chokepoint categories and offers mitigation playbooks, from dual-sourcing to strategic inventory hedges.

Competitive landscape: what incumbents are doing — and where gaps remain

Our competitor analysis profiles leading engine and powertrain players and distils where each has structural advantages or exposure in 2026:

-

Cummins Inc. continues to emphasize platform breadth and emissions integration, bringing next-generation off-highway engine variants to major trade shows in early 2026. Their strengths include deep systems integration and service networks, making them a natural partner for OEMs seeking modular powertrain packages.

-

Volvo Penta retains a value proposition built on robust industrial engines and credibility in marine and off-highway segments; their product architecture supports high durability and aftermarket support for demanding duty cycles.

-

John Deere balances in-house engine development with vertical integration into equipment platforms, leveraging application-specific knowledge in agriculture and construction to tune power and emissions trade-offs.

-

Yanmar is notable for compact, high-efficiency packages and early hybrid implementations — positioning them well in applications where footprint and fuel efficiency are decisive.

-

DEUTZ AG and MAN / Traton offer complementary strengths in mid- to high-power ranges and custom industrial solutions; they are visible at major industry exhibitions in 2026, underscoring their go-to-market intent.

-

Caterpillar and Kohler remain anchors for high-power heavy equipment and off-highway engines, with deep installed bases that support aftermarket service and retrofit opportunities.

Across this competitive set, PW Consulting identifies recurring strategic gaps: limited scaled offerings for coordinated hybrid + aftertreatment systems in certain duty cycles, uneven service & telematics propositions in emerging markets, and varied preparedness for the potential timing of the most stringent emissions standards.

Recent events that change 2026 priorities

-

Industry showcases in early 2026 — with multiple OEMs exhibiting next-gen off-highway engine platforms — have accelerated benchmarking activity and supplier selection processes for major equipment manufacturers.

-

Regulatory developments (notably draft Tier 5-level proposals targeting up to ~90% NOx reductions in the coming decade) introduce a multi-year compliance runway that companies must now model explicitly into product and capital plans.

-

Ongoing certification guidance updates for small engines create immediate implications for suppliers who service small off-road equipment OEMs, influencing product certification timetables and inventory strategies.

What PW Consulting’s report delivers — practical contents for commercial execution

The report is designed as an execution toolkit, not just a forecast. Key deliverables include:

-

Portfolio prioritization matrices that map product variants to duty cycles, profitability and regulatory risk.

-

Scenario-based financial models (TCO and NPV) for powertrain choices across a range of fuel and emissions cost assumptions.

-

Regulatory impact playbooks showing phased compliance costs and recommended technology mixes under alternative policy timelines.

-

Supplier and component risk heat maps, with mitigation levers and sourcing strategies tailored to supplier concentration profiles.

-

M&A screening frameworks and a shortlist of archetypal targets for capability buys — electrification, aftertreatment, and digital service platforms — aligned to different buyer profiles.

-

Commercial go-to-market designs for service, telematics and powertrain-as-a-service propositions that increase annuity revenue and reduce fleet TCO.

Each toolkit element is linked to underlying dataset extracts and sensitivity analyses; however, the full segmented datasets (regional and application splits) and proprietary unit-cost schedules are available only in the complete report.

Actionable recommendations for 2026

-

Prioritize modularity: Invest in modular engine and aftertreatment architectures to preserve commonality across platforms while meeting staggered emissions timelines. This reduces rework costs as standards tighten.

-

Stress-test regulatory timing: Run alternate compliance timelines (accelerated and delayed) through decision gates for product launches, capex and procurement contracts to avoid stranded assets.

-

Lock down critical components: Identify top-tier suppliers for aftertreatment and power electronics and secure medium-term contracts or equity stakes in those suppliers to reduce supply volatility.

-

Design for service monetization: Build telematics-enabled service bundles that convert one-time sales into recurring annuity streams, improving customer retention and smoothing demand cycles.

-

Targeted M&A and JV plays: Acquire or partner for gaps in hybridization, energy storage and digital service capabilities rather than attempting in-house development in all domains.

-

Operationalize emissions intelligence: Embed regulatory scenario dashboards in product planning to make compliance a quantifiable input in R&D prioritization and pricing models.

Conclusion — how PW Consulting helps you move from insight to execution

For leaders making allocation and product decisions in 2026, the off-road engines market presents both persistent demand drivers and sharply rising compliance costs. PW Consulting’s report turns the complexity of regulation, technology diffusion and supply concentration into clear, prioritized action sets paired with the underlying data and models. We intentionally present a calibrated preview here to show the study’s depth while preserving the detailed, proprietary segmentation and unit-level economics that differentiate our advisory work.

To access the full set of datasets, scenario models, and the complete competitive scorecards — including the regional and application-level insights necessary for precise market entry or divestiture planning — download the full report at PW Consulting’s Off-road Engines Market page.

For detailed analysis of this topic, please visit the official page: Off-road Engines Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com