@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting: CO2 Market Set to Grow at a 3.6% CAGR from 2026–2032

Carbon Dioxide (CO2) Market 2026 Intelligence: Strategic Implications for Corporate Decision‑Makers

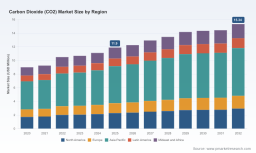

PW Consulting’s latest Carbon Dioxide (CO2) Market report—anchored on a 2025 base year and offering a 2026–2032 forecast—translates evolving supply, demand and regulatory dynamics into pragmatic strategic options for corporate leaders. The global market has shown steady expansion in recent years, evolving from roughly USD 9.0 Million in 2020 to USD 11.9 Million in 2025, and our forecast points to continued growth at a compound annual growth rate (CAGR) of 3.6% through 2032 (reaching approximately USD 15.3 Million by 2032). For executives preparing 2026 capital allocation, procurement and M&A decisions, this research functions less as a static number set and more as an operational playbook for navigating complexity.

Carbon Dioxide (CO2) Market

Why the 2026 Planning Cycle Demands Fresh CO2 Market Intelligence

-

Policy shifts have become direct cost drivers. New trade and carbon regulatory regimes are already translating into measurable input‑cost volatility and shifting sourcing advantages across jurisdictions.

Carbon Dioxide (CO2) Market -

Structural supply adjustments—driven by plant retirements, consolidation among major industrial gas suppliers, and changes in feedstock availability—are compressing near‑term flexibility in merchant CO2 supply chains.

Carbon Dioxide (CO2) Market -

End‑market transitions (from food & beverage cold‑chain optimization to industrial gas substitution in select chemical processes) are changing demand profiles for gaseous CO2, liquid CO2 and dry ice, creating both risk and arbitrage opportunities for incumbent suppliers and new entrants.

Market Trajectory: What the Numbers Mean for Strategy

The market’s mid‑single‑digit CAGR masks important strategic nuance. A steady increase in overall market value to USD 11.9 Million in 2025 confirms persistent baseline demand; however, evolution in regional regulation, production capacity and carbon pricing will re‑shape margins and contract structures. A 3.6% CAGR through 2032 does not imply uniform growth across product forms, customer segments or geographies. For boardrooms and corporate development teams, the takeaways are clear:

-

Plan for steady, not spectacular, topline growth but heightened margin dispersion driven by carbon policy and supply constraints.

-

Prioritize operational resilience—redundant sourcing, dynamic contract terms, and inventory strategies (including dry ice logistics) will have an outsized impact on 2026 P&L variability.

-

Factor carbon‑cost pass‑through and border mechanisms into pricing models: companies that can model and hedge these variables will outperform peers when volatility spikes.

Near‑Term Dynamics to Watch in 2026

The report synthesizes several contemporaneous developments that will directly influence 2026 decisions:

-

Regulatory regime shifts: The EU’s Carbon Border Adjustment Mechanism (CBAM) entered its definitive stage at the start of 2026, altering import cost structures for covered goods and creating an immediate need for importers and their CO2 suppliers to re‑price contracts and reassign logistics costs along value chains.

-

Domestic capacity changes: U.S. merchant CO2 nameplate capacity has shown contraction compared to the prior year, largely due to plant closures—an operational reality that tightens merchant availability and raises the strategic value of long‑term supply agreements and bilateral offtake arrangements.

-

Effective carbon pricing: Elevated effective carbon rates across the EU (reported in the range of €70–75 per tonne in 2025) are now a near‑term cost input for industrial gases, affecting both production and customer pricing strategies.

Supply Chain & Production Implications

CO2 supply chains are increasingly characterized by a mix of long‑tenor contractual commitments, on‑demand merchant channels, and integration with adjacent product streams (dry ice, refrigeration services). Our analysis finds that strategic responses fall into three operational buckets:

-

Contract portfolio optimization: Sophisticated buyers are shifting toward blended portfolios (firm long‑term supply + flexible spot access) to balance security and price exposure.

-

Localization and redundancy: Firms with geographically distributed production or multi‑modal logistics options (rail, bulk tanker, cylinder networks) are better positioned to absorb regional shocks from plant outages or regulatory disruptions.

-

Feedstock & by‑product value capture: Refinery and ethanol plant closures or ramp‑downs alter merchant supply flows; companies that can secure co‑production linkages or retrofit capture systems achieve supply advantages.

Commercial Opportunities — Where to Compete

The market’s structural features create differentiated opportunities for incumbents and challengers alike:

-

Contracting innovations: Suppliers that can offer transparent carbon‑cost indexing, pass‑through mechanisms tied to carbon allowance pricing, or supply‑chain audits that validate CO2 provenance, will win procurement share among carbon‑sensitive buyers.

-

Value‑added service models: Combining CO2 supply with downstream services (cold‑chain optimization, on‑site inventory management, dry‑ice delivery programs) raises switching costs and improves margin capture.

-

Niche playbooks: Targeted offerings for high‑margin end uses (e.g., certain food processing, specialty industrial applications, and medical uses) allow premium pricing and contractual protections.

Competitive Landscape: Profiles & Strategic Signals

We profile the incumbent industrial‑gas players whose strategic moves shape supply and commercial norms:

-

Linde plc (Woking, UK): A global leader in industrial gases, Linde continues to deepen long‑term offtake relationships tied to low‑carbon production projects—contributing to supply security for large offtakers while signaling elevated barriers for pure merchant players.

-

Air Liquide S.A. (Paris, France): Through its integration initiatives and established distribution networks, Air Liquide is consolidating scale advantages in bulk and packaged CO2 delivery and capitalizing on customer consolidation in major markets.

-

Air Products and Chemicals, Inc. (Allentown, PA, USA): With strong capabilities across cooling and dry‑ice products, Air Products remains a key supplier for industrial, medical and food customers where thermal properties and logistics are critical.

-

Airgas USA, LLC (Radnor, PA, USA): As a leading U.S. distributor, Airgas’ depth in cylinders, bulk and localized service networks positions it as a tactical partner for U.S. manufacturing and food service customers.

Recent strategic developments underscore market direction: Linde’s long‑term supply agreement with a low‑carbon ammonia project in Louisiana signals a trend toward integrated, decarbonized supply chains; Air Liquide’s celebration of a decade of integration in the U.S. underscores the strategic benefits of scale in distribution and customer footprint. These moves reduce merchant channel elasticity and raise the strategic cost for late movers.

How PW Consulting’s Report Translates into 2026 Actions

Our report is purpose‑built for decision cycles that require immediate, implementable conclusions. Key deliverables include:

-

Probabilistic supply‑demand model that allows scenario testing against alternative carbon‑price and capacity outcomes—enabling procurement teams to stress‑test contract structures under CBAM and elevated carbon allowances.

-

Procurement playbook with recommended contract clauses for price indexation, force majeure, and takeover rights—designed to be inserted into RFPs within 60 days of engagement.

-

Investment screen for M&A and capacity expansion that ranks opportunities by strategic fit, capital intensity and expected timeline to first cash flow under multiple regulatory regimes.

-

Operational checklist for supply resilience—covering dual‑sourcing triggers, inventory thresholds for dry ice and bulk CO2, and logistics contingency plans that link to enterprise risk management frameworks.

-

Competitive scorecards and supplier negotiation templates—enabling commercial teams to convert market intelligence into improved margin and service KPIs.

Risk Matrix & Scenario Drivers

The report delineates a compact risk matrix mapped to probability and impact across four vectors: regulatory (trade and carbon border rules), capacity (plant closures and feedstock swings), price (carbon and logistics cost pass‑through), and market structure (consolidation among top suppliers). Each vector is accompanied by early‑warning indicators that executives can operationalize in 90–120 day intelligence cycles.

What We Deliberately Withhold from This Executive Summary

Following our “trailer” approach, this public summary highlights the analytical framework and strategic conclusions while withholding granular regional and application splits, detailed supplier share tables, and full numeric scenario outputs. These are included in the full report and are essential for transactional‑level decisions such as tender pricing, granular hedging programs, and jurisdiction‑specific capital planning.

For Boards, CFOs and Commercial Leaders: Immediate Next Steps

-

Integrate carbon pricing into 2026 procurement scenarios: update models with CBAM and local effective carbon rates and run at least three supply sensitivity scenarios before contract renewals.

-

Reclassify supply risk using our capacity indicators: identify single‑point‑of‑failure suppliers and secure secondary contracts for critical sites.

-

Assess M&A targets and partnerships: prioritize assets that provide logistical reach or low‑carbon certificates that materially reduce CBAM exposure.

-

Deploy the report’s contracting templates in upcoming RFPs to realize near‑term margin protection.

To access the full dataset, granular regional and application breakouts, supplier share tables, and executable templates described above, download the complete PW Consulting Carbon Dioxide (CO2) Market report on our website. The full report contains the proprietary models and annexes required for implementation and transactional decision‑making in 2026.

For detailed analysis of this topic, please visit the official page: Carbon Dioxide (CO2) Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com