@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting: Industrial Door Sensing Devices Market to Climb from USD 179.5 Million in 2025 to USD 247.2 Million by 2032, Posting a 4.8% CAGR (2026–2032)

Industrial Door Sensing Devices Market — Strategic Imperatives for 2026

Executive snapshot

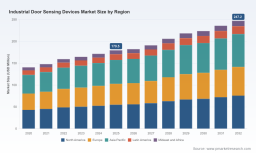

PW Consulting today releases a forward-looking briefing built from our latest Industrial Door Sensing Devices Market study (base year 2025, historical 2020–2025, forecast 2026–2032). The market has expanded steadily from a clearly defined 2020 baseline and reached an estimated USD 179.5 million in 2025. Under our central scenario the market progresses to roughly USD 247.2 million by 2032, reflecting a compound annual growth rate (CAGR) of approximately 4.8% across the 2026–2032 forecast window.

Industrial Door Sensing Devices Market

For executives calibrating product investments, procurement strategies, or M&A activity in 2026, the report is designed as a practical decision-support toolkit: it combines rigorous, auditable macro-sizing with scenario-led strategic options, supplier scorecards, implementation checklists and regulatory impact mapping. This release note highlights the report’s unique strategic value while intentionally reserving granular split data to the full report — a focused preview that shows what matters and directs readers to the source for the detailed KPIs that power execution.

Industrial Door Sensing Devices Market

Why this market matters in 2026

-

Risk and regulation are converging with automation. Global and regional safety standards (including long-standing references such as UL 325 and recent regulatory clarifications used in North America and elsewhere) continue to push owners and integrators toward certified sensing solutions and continuous monitoring architectures.

Industrial Door Sensing Devices Market -

Warehousing and logistics modernization — accelerated by e-commerce and shoring-up supply chains — is increasing the aftermarket and retrofit opportunity for industrial door sensing systems. Facilities investing in throughput and worker safety see sensing devices as low-friction, high-ROI control points.

-

Technology shift: the unit is not just a sensor. Buyers increasingly expect connectivity, diagnostic telemetry, OTA firmware, and secure interfaces with building automation and access control. This is opening margin pools for suppliers that can pair hardware with subscription services.

-

Market structure is meaningful. The market is concentrated among a handful of established specialists, creating both barriers and platforms for new entrants. Our concentration analysis shows that the top three and top five suppliers command a materially large share of revenues — a factor that informs competitive and partnership strategies.

What the PW Consulting report delivers (practical content)

-

Rigorous market sizing and validated forecasts across 2026–2032, with sensitivity and scenario pathways (base, accelerated adoption, and conservative investment scenarios) so leaders can stress-test capital plans.

-

Actionable demand-driver analysis — mapping how regulatory timelines, retrofit cycles, and distribution center expansion translate to near-term (12–24 month) purchase windows.

-

Supplier scorecards and capability maps — independently assessed on technical performance, compliance maturity, channel reach, and service model. These are complemented by RFP templates and negotiation playbooks.

-

Technology & integration playbook — comparison of sensing modalities (active infrared, LiDAR-like scanning, radar, ultrasonic, mechanical contact edges, etc.) by use-case suitability, installation complexity, and total cost of ownership (TCO) implications.

-

Regulatory impact matrix and implementation checklist that aligns standards (UL 325, CPSC rules relevant to entrapment mitigation, occupational safety norms such as ISO 45001) to procurement and test procedures.

-

Commercial benchmarks — pricing guidance, warranty and service models, upgrade paths and suggested bundling strategies for hardware + software revenue capture.

-

M&A and partnership playbook focused on three archetypes: capability acquisition (edge compute, analytics), channel expansion (regional distributors and integrators), and product-line bolt-ons (retrofit kits and modular sensors).

Competitive landscape — who matters and why

The industry remains populated by a mix of specialist sensor manufacturers and broader industrial automation firms. Our competitive analysis highlights five firms that shape product direction, channel behavior and standards interpretation:

-

Hotron (Japan) — a focused automatic-door sensor specialist known for compact activation and safety devices tailored to sliding and swing door use-cases. Recent product activity through late 2025 and into 2026 underscores Hotron’s strategy of incremental, installer-friendly innovation: multi-function activation/safety sensors and targeted upgrades that accelerate installation time and reduce labor costs.

-

BEA Sensors (United States) — established for motion, presence and safety scanners and curtain sensors for high-speed doors and loading-dock scenarios. BEA’s product family — including scanning and presence detection models — positions it strongly with warehouse and logistics integrators where throughput and pedestrian protection are priorities.

-

OP TEX (Japan) — emphasizes high-performance detection and pedestrian safety in commercial and industrial contexts. Their engineering focus on reliability and precision detection under variable environmental conditions is an anchor for customers prioritizing uptime.

-

Telco Sensors (Germany) — a European presence manufacturing presence and safety devices, with strengths in meeting local installation practices and distributor relationships across industrial markets.

-

ifm electronic (Germany) — broader industrial automation portfolio with fail-safe inductive sensors and RFID-coded safety switches that frequently serve integrators seeking turnkey reliability and compatibility with factory automation systems.

PW Consulting’s supplier assessments combine objective lab performance tests, channel checks and commercial interviews. The full report contains comparative scorecards and procurement-ready evaluations designed for CIOs, CTOs, procurement heads and M&A teams. In the spirit of this preview, we highlight patterns rather than granular ranks: large, specialized vendors retain advantages in product certification and distribution; mid-tier players are competing on integration and service models; and niche entrants win by delivering software-enabled value propositions.

Near-term strategic plays for 2026

-

Prioritize retrofit-friendly product lines. For owners of aging door fleets the fastest path to risk reduction and compliance is modular sensor solutions with minimal structural work. Allocate CapEx to kits that reduce installation labor.

-

Invest in connected diagnostics. Even modest telemetry that reduces site visits can move a sensing-device purchase from a commodity buy to a recurring-service revenue stream. For manufacturers, build secure, standards-aligned APIs from day one.

-

Use regulatory timelines as a sales lever. Buyers respond to compliance requirements; procurement and channel teams should align marketing, training and certification support with the most relevant standards in target regions.

-

Adopt a portfolio approach to supplier selection. Combine incumbent-certified vendors for critical safety devices with niche partners for advanced sensing or analytics — this reduces single-vendor risk without sacrificing performance.

-

Prepare supply continuity plans for critical components. Component concentration in sensing (for example, certain optoelectronic modules) can create pinch points. Design products with component flexibility and qualify alternate suppliers in 2026.

-

Pursue tuck-in M&A to accelerate software and connectivity capabilities. Targets that enable remote diagnostics, predictive maintenance or firmware management materially lift margins and create cross-sell opportunities.

How to use this report for immediate impact

-

Run 90-day vendor audits using our supplier checklist to identify certification and service gaps that elevate near-term safety risk.

-

Apply the included scenario models to board-level capital planning to see how different adoption speeds alter ROI and payback timelines.

-

Leverage the RFP templates and scoring matrices in supplier negotiations to secure performance guarantees and post-sale service credits.

-

Integrate the regulatory impact matrix into procurement and project specifications so that safety and compliance are contractual deliverables, not afterthoughts.

Closing — why PW Consulting’s insight matters for 2026

Between 2026 and 2032 the industrial door sensing devices market is expected to follow a steady, predictable growth path. That predictability masks complexity: growth is uneven by use-case and distribution channel, influenced by regulatory cycles, retrofit economics and technology transitions from basic sensing to connected, software-rich systems. PW Consulting’s report synthesizes these forces into decision-ready guidance for executives who need to convert market forecasts into procurement plans, product roadmaps and M&A pipelines in 2026.

If your organization is preparing to invest, partner, or compete in this space, the full report delivers the granular split tables, vendor scorecards, pricing benchmarks and downloadable tools required to operationalize strategy. PW Consulting invites procurement teams, product leaders and corporate development groups to review the complete study and use our templates to accelerate decision velocity in 2026.

For detailed analysis of this topic, please visit the official page: Industrial Door Sensing Devices Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com