@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting Forecasts Retail Bank Loyalty Program Market to Grow from USD 215.0 Million in 2025 to USD 344.8 Million by 2032 at a 6.0% CAGR

Retail Bank Loyalty Program Market — Strategic Preview for 2026 Decision-Makers

PW Consulting today publishes a strategic preview of our forthcoming Retail Bank Loyalty Program Market report (base year 2025), designed to equip executive teams with the actionable insight they need to make defensible investments and product choices in 2026. The market for retail banking loyalty solutions has evolved from a niche, promotional tool into a core customer engagement lever. Our analysis combines a five-year historical view (2020–2025) with a forward-looking forecast through 2032, offering both the empirical baseline and scenario-driven pathways for banks and solution providers.

Retail Bank Loyalty Program Market

Market snapshot: scale and trajectory

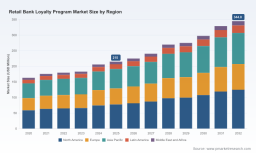

Key macro metrics underscore why loyalty programs are rising on boardroom agendas. The global retail bank loyalty solutions market expanded from approximately USD 163.2 million in 2020 to USD 215.0 million in 2025, reflecting steady adoption and incremental product sophistication. We project continued growth at a compound annual growth rate (CAGR) of 6.0% through the 2026–2032 forecast window, culminating in an expected market size near USD 345 million by 2032 under our baseline scenario.

Retail Bank Loyalty Program Market

Those headline figures mask a deeper structural shift. Early-stage deployments were characterized by transactional rewards and partner networks; the next wave is driven by data-enabled personalization, embedded payments, and platform-grade integrations that scale across digital channels. For strategists evaluating 2026 resource allocations, the takeaway is clear: loyalty is no longer a marketing adjunct — it is an experience platform that directly affects acquisition, retention, and interchange economics.

Retail Bank Loyalty Program Market

Why this matters for 2026 planning

- Investment timing: With mid-single-digit CAGR and compounding benefits from cross-sell and retention, 2026 is the inflection point to move from pilot to platform. Early adopters converting pilots into bank-wide programs in 2026 will capture disproportionate lifetime value as maturity premiums widen.

- Technology choices: Cloud-native architectures, AI-driven decision engines, and modular APIs are the operational enablers of scale. Firms that select composable solutions in 2026 avoid costly rewrites and gain faster time-to-market for partner integrations.

- Operational ROI: Loyalty programs increasingly intersect with payments, digital wallets, and card schemes. The financial benefits are realized through improved spend retention and reduced attrition—metrics that should be monetized in 2026 business cases to secure budget and executive sponsorship.

- Competitive posture: Market concentration data shows a moderately consolidated vendor landscape (CR3 ~50%; CR5 ~60%). This signals both the dominance of established providers in enterprise-grade implementations and opportunity for niche specialists with differentiated propositions.

Regulatory and risk dynamics shaping product design

Designing loyalty programs for banks in 2026 requires navigating a tightening regulatory environment and elevated security expectations. Key constraints and enablers identified in our research include:

- Data privacy and consent: GDPR-style regimes and local privacy laws constrain third-party data sharing and require granular consent flows. Vendors and banks must embed privacy-by-design into loyalty architectures to sustain personalization without regulatory friction.

- KYC and fair-lending considerations: Loyalty mechanics must be reconciled with KYC obligations and anti-tying laws, particularly when rewards are linked to credit products or conditional benefits.

- Fraud detection and AI oversight: Banking-grade programs demand robust AI tools to detect loyalty fraud and prevent gaming. Our report benchmarks the technical controls that should be in place and outlines an audit framework for model governance.

- Cloud and integration compliance: Modern loyalty deployments favor multi-tenant cloud infrastructures with certified controls. The right cloud strategy balances scalability with jurisdictional data residency and regulatory reporting requirements.

Competitive landscape — strategic implications for banks and vendors

Our competitive analysis profiles a diverse set of providers, ranging from full-suite platform vendors to specialized loyalty engines. Two exemplar vendors illustrate distinct strategic approaches relevant to 2026 decision-making:

- Comarch SA (Krakow, Poland) — Comarch’s loyalty marketing solution targets banks seeking an enterprise-grade, cloud-hosted platform. Its offering is notable for integrating AI-driven personalization, gamification modules, tiered reward structures, partner ecosystem management, and embedded fraud detection. For banks prioritizing security and compliance while wanting a rich feature set out of the box, Comarch represents a low-friction path to scale. Considerations for 2026: evaluate their integration templates and SLAs for regional compliance variation, and stress-test AI models against expected transaction volumes.

- Antavo (Tallinn, Estonia) — Antavo positions itself as a flexible loyalty engine with an emphasis on no-code campaign workflows, a digital wallet layer, and sophisticated tier/segment management. Their platform is architected for rapid personalization and marketer-driven campaign control, which reduces time-to-value for CRM teams. Considerations for 2026: measure the extent of banking-specific compliance tooling (KYC, audit trails), and validate resiliency under high-concurrency events like product launches.

Both vendor archetypes are well-represented among enterprise deployments. The strategic decision for banks in 2026 is less binary and more contingent: do you prioritize operational control and marketing agility (no-code, headless engines), or is banking-grade security, partner onboarding and deep fraud-detection the primary selection criterion? The optimal path for many institutions is a hybrid approach — core banking-integrated loyalty modules combined with marketing-layer flexibility.

Real-world movement — ecosystem partnerships and learnings

Recent developments validate our thesis that partnerships and ecosystem plays will accelerate in 2026. An illustrative example: in May 2026 Scotiabank expanded its Scene+ program with a major fuel retailer, enhancing everyday value propositions for debit and credit users across a wide retail footprint. Such moves demonstrate two points relevant to 2026 strategists: first, co-branded and merchant-linked rewards materially increase program utility; second, partnerships require robust settlement, fraud controls, and partner onboarding processes that must be part of the implementation plan.

What the PW Consulting report contains — practical deliverables (preview)

Our full report goes beyond descriptive analysis and provides operationally focused tools intended for immediate use in 2026 program planning:

- Executive decision frameworks for build vs. buy assessments, with scoring models that weight compliance, total cost of ownership, and speed to market.

- A vendor diligence checklist and RFP template tailored to banking requirements, covering data residency, ML governance, auditability, and partner settlement capabilities.

- Implementation blueprints for integrations with core banking, payments rails, and digital wallets, including recommended API patterns and fallback strategies.

- Program design modules — loyalty mechanics, tier strategies, partner revenue-sharing models — with measured KPIs and sensitivity analyses for retention and lifetime value uplift.

- Regulatory compliance playbook summarizing privacy, KYC, anti-tying and model-validation steps necessary to operate at banking scale.

- An ROI and scenario modelling workbook that helps quantify expected payback under conservative/central/accelerated adoption cases.

Importantly, the report contains comprehensive segmentation and granular market datasets (by region, type and application), vendor profiles, and forecasted scenarios. In keeping with our “trailer” approach for this press release, we intentionally withhold detailed segment tables here: these datasets are central to the full deliverable and available on the report page for licensed subscribers.

Actionable guidance for 2026 executive agendas

- Prioritize modularity: Composable platforms decouple marketing innovation from core banking risk, enabling rapid campaigns without exposing regulated systems.

- Govern your AI: Deploy model governance from day one — logging, explainability and human-in-the-loop controls will be procurement requirements and regulatory expectations.

- Lock down partner operations: Channel and merchant integrations scale complexity; dedicate a partner operations function to manage onboarding, settlement and fraud monitoring.

- Measure the right KPIs: Emphasize LTV uplift, spend retention, and net promoter movement rather than vanity metrics; align rewards to measurable revenue levers.

- Plan for composable compliance: Embed privacy and consent mechanisms into the loyalty data fabric to sustain personalization without regulatory risk.

Closing — why the 2026 moment matters

As the market shifts from isolated promotional mechanics to platform-level engagement, the decisions made in 2026 will lock in strategic trajectories for the decade. With a market growing from roughly USD 163 million in 2020 to USD 215 million in 2025 and projected to reach near USD 345 million by 2032 at a 6.0% CAGR, the economics favor well-governed, scalable programs. Firms that get the architecture, governance and partner play right will gain outsized customer economics; those that delay risk being relegated to tactical, low-margin programs.

PW Consulting’s full Retail Bank Loyalty Program Market report provides the datasets, frameworks, and implementation tools to act with confidence in 2026. For decision-makers who require the full segmentation, vendor scorecards, and downloadable toolkits, please visit the report page to request access and license the complete analysis.

For detailed analysis of this topic, please visit the official page: Retail Bank Loyalty Program Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com