@pmarketresearch

- Followers 0

- Following 0

- Updates 57

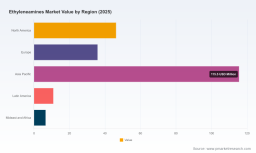

PW Consulting: Ethyleneamines Market to Grow from USD 215.0 Million in 2025 to USD 344.8 Million by 2032 at 5.41% CAGR — Asia Pacific Leads with USD 115.5M, Top 3 Hold 42.5%

Ethyleneamines Market: Strategic Briefing for 2026 Decision-Makers

Executive Summary

PW Consulting’s latest market study on Ethyleneamines delivers a concise, strategy-first synthesis of an industry transitioning from chemical-commodity dynamics toward sustainability-driven differentiation. Built on a base year of 2025 and covering historical performance from 2020–2025 with a forecast horizon of 2026–2032, the report quantifies a consistent mid-single-digit growth trajectory (CAGR 5.41%). In simple terms: the global ethyleneamines market has expanded from the low hundreds of USD Million in 2020 to an estimated USD 215.0 Million in 2025 and is forecast to continue climbing through the projection period, reflecting steady demand across industrial intermediates, curing agents, and specialty chemistries.

Ethyleneamines Market

Why this report matters for 2026 decisions

-

Timing: 2026 is the inflection year for many strategic choices—capex commitments, portfolio rebalancing, and supplier contracts—because the industry is consolidating technological, regulatory, and feedstock shocks into lasting structural change.

Ethyleneamines Market -

Risk-reward balance: Supply disruptions and sustainability certifications are changing the risk profile for incumbents and entrants alike. Our analysis isolates the channels through which those shocks flow to margins and availability.

Ethyleneamines Market -

Actionability: The study is structured to convert market intelligence into decision-ready scenarios—helping procurement, R&D, and corporate development teams prioritize investments and hedges.

Market snapshot (high-level)

Across the historical window (2020–2025) the market exhibited resilient growth, reaching an estimated USD 215.0 Million in 2025. Under our base modeling assumptions, the market continues to expand through the forecast period to 2032, driven by steady demand in industrial applications and incremental adoption in specialty downstreams. The calculated compound annual growth rate for the forecast horizon is 5.41%, a pace that supports both organic capacity additions and selective strategic investments.

Competitive structure and concentration

The market remains moderately concentrated: the top three global producers account for a meaningful share of industry shipments, and the top five materially increase that concentration. That concentration profile creates strategic levers (e.g., price leadership, capacity coordination) and entry hurdles (scale, feedstock securement) for potential entrants. Our report quantifies concentration metrics and models their sensitivity to new capacity and demand shocks, enabling buyers and sellers to stress-test scenarios for 2026 planning.

Recent industry dynamics that change strategic calculus

-

Sustainability certification is now a commercial asset. The first mainstream ISCC PLUS certifications for green ethylene oxide and derivatives have been granted, enabling traceable supply chains for low-carbon feedstocks. Firms with certified supply chains stand to capture premium demand from sustainable downstream segments.

-

Supply shocks remain a material risk. Recent force majeure events tied to upstream cracker outages have highlighted the fragility of mixed-feed supply chains and the need for contingency strategies in procurement and inventory management.

-

Capacity and modernization investments continue. Leading producers have announced both capacity expansions and multi-million dollar modernization programs aimed at improving energy efficiency and production flexibility—moves that will reshape regional cost curves and commercial bargaining power over the next 18–36 months.

-

Regulatory and process approvals for novel production technologies are accelerating. New process approvals in major jurisdictions lower execution risk for technology-led operators, creating windows for first-mover advantage in lower-emission assets.

Strategic implications — seven priorities for 2026

-

Supply-chain resilience and dual-sourcing: The 2025 supply interruptions demonstrate the value of multi-origin sourcing and strategic safety stocks. Companies should deploy scenario-based procurement playbooks that balance working capital against service-level risk.

-

Certification and green feedstocks as commercial differentiators: Buyers, especially in specialty and regulated sectors, will increasingly prefer certified inputs. Firms should evaluate certification pathways (and the capex/Opex needed to achieve them) as market access investments rather than compliance costs.

-

Selective capacity vs. partnerships: Given moderate market concentration, greenfield capacity is viable for scale players but high-risk for smaller entrants. Joint ventures, tolling agreements, and off-take contracts can be effective alternatives to de‑risk expansion while preserving market optionality.

-

Product and margin management: Portfolio optimization—shifting toward higher-margin specialty amines and application-specific formulations—can insulate revenues from commodity price swings. R&D prioritization should align with end-market pull and regulatory tailwinds.

-

Pricing and contract sophistication: Implement blended contracting strategies that combine index-linked elements with fixed-volume hedges to capture upside while protecting against feedstock scarcity-driven spikes.

-

M&A and consolidation playbooks: Mid-sized strategic acquisitions that add regional footprint or specialized chemistries offer immediate scale benefit in a moderately concentrated market; conversely, divestitures of low-margin commodity streams can free capital for sustainability investments.

-

Operational modernization and energy efficiency: Plant upgrades that lower energy intensity and broaden feedstock flexibility will pay back more quickly under current and anticipated regulatory regimes; prioritize projects with the quickest IRRs aligned to emission reduction targets.

Competitive landscape — who matters and why

Global and regional leaders maintain a mix of commodity-scale production and targeted specialty portfolios. Key players include integrated chemical majors, focused specialty producers, and merchant suppliers. These firms differ in feedstock strategies, geographic footprint, and product breadth—factors that determine their vulnerability to upstream shocks and their ability to capture premium, certified demand. PW Consulting’s report provides a tactical analysis of each major competitor, assessing their capacity posture, certification status, recent strategic moves, and the implications for customers and competitors in 2026.

Report contents — what you get (practical details)

-

Market-sizing and trend decomposition: Annualized market data from 2020 through 2025, plus a rigorously modeled outlook to 2032 with scenario bands that reflect alternative macro, feedstock, and regulatory outcomes.

-

Granular demand drivers and end-market mapping: Application-level demand drivers, cross-elasticities, and adoption curves that feed into product strategy and go-to-market planning. (Note: this briefing omits detailed segment shares to preserve the “trailer” function—full segmentation is available in the report.)

-

Supply-side intelligence: Capacity maps, utilization analysis, and a risk register for feedstock and logistic constraints—useful for capex timing decisions and contract structuring.

-

Competitive playbook: Profiles of leading producers and emerging players, annotated with recent developments, strategic intentions, and tactical recommendations for suppliers and buyers.

-

Scenario planning toolkit: Decision trees and playbooks for procurement, R&D investment, M&A screening, and regulatory compliance pathways, calibrated to the forecasted CAGR and concentration dynamics.

-

Implementation annexes: Model templates, procurement checklist, and a 90/180/360-day tactical roadmap to operationalize findings within a corporate planning cycle.

How procurement, R&D and corporate development should use this

-

Procurement: Use the supply-risk scoring in the report to re-prioritize suppliers and negotiate flexible terms that incorporate sustainability premiums and force majeure clauses reflective of recent market reality.

-

R&D: Align product roadmaps with downstream customers’ sustainability commitments and the identified mid-term demand pockets—invest where technical differentiation yields durable margin expansion.

-

Corporate Development: Employ the M&A filters and valuation sensitivity models to screen targets that accelerate access to certified feedstocks, specialized formulations, or strategic regional footholds while avoiding low-return commodity buildouts.

Call to action

PW Consulting’s Ethyleneamines Market report is designed to be a decision-ready tool for 2026 planning cycles. It combines market math (historical series through 2025, forecast to 2032, and a 5.41% CAGR), competitive intelligence, and tactical playbooks to convert insights into mapped actions. For commercial teams, risk officers, and investment committees preparing decisions this year, the report provides both the macro prism and the operational checklists necessary to act with confidence.

To access the full dataset, segmented modelling, and proprietary scenario tools referenced in this briefing, visit PW Consulting’s report page and download the complete study. The full report contains the segment-level detail and model workbooks required to operationalize the strategic recommendations summarized here.

For detailed analysis of this topic, please visit the official page: Ethyleneamines Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com