@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting: Global Tape Measures Market Poised to Reach USD 296 Million by 2032, Supported by a 4.75% CAGR

Tape Measures Market 2026 Strategic Brief: What Every Executive Needs to Know

As PW Consulting’s lead industry analyst, I present the executive summary of our Tape Measures Market report — the actionable intelligence designed to shape 2026 corporate decisions. Built on a 2025 base year and a seven‑year forecast horizon (2026–2032), the market shows a steady expansion driven by professional trades, product innovation, and regulatory tightening. Our forecast projects the market to grow from an estimated USD 215.0 Million in 2025 to roughly USD 296.0 Million by 2032, reflecting a compound annual growth rate (CAGR) of 4.75% (currency: USD, revenue unit: Million). Market concentration is meaningful but not prohibitive (top‑three firms account for mid‑30s percent of sales; top‑five approaches the mid‑40s percent), leaving room for both scale plays and differentiated niche strategies.

Tape Measures Market

Why this report matters for 2026 decisions

- It translates macro growth into operational choices: product investments, channel prioritization, procurement strategy, and compliance budgeting.

- It identifies where incremental investments yield outsized returns — for example, blade technology, hook systems, and professional‑grade durability that drive premiumization in the trade channel.

- It highlights regulatory and supply‑chain variables that can materially affect gross margins and time‑to‑market in 2026.

- It structures M&A and partnership targets in a market that is consolidated enough for scale, yet fragmented enough for bolt‑on acquisitions to create value.

Macro trajectory and on‑the‑ground implications

The tape measures market recovered and expanded through the historical window (2020–2025), propelled by renewed construction activity, woodworking demand, and replacement cycles in professional tool kits. The projected 4.75% CAGR to 2032 translates into a predictable, investible growth corridor rather than an episodic boom — an environment where disciplined product roadmaps and efficient route‑to‑market execution win.

Tape Measures Market

For manufacturers and brand owners, this means prioritizing incremental innovation and operational excellence over speculative, high‑capex gambits. Expect steady demand for both traditional steel tapes and fiberglass offerings, coupled with an increasing willingness among professional buyers to pay for measurable performance (durability, accuracy, ease of use) and verifiable certification.

Tape Measures Market

Competitive landscape: positioning and strategic implications

The competitive field is a mix of global incumbents, precision specialists, and manufacturing‑scale producers. Each group faces distinct strategic imperatives in 2026:

- Global incumbents and generalist tool majors — companies with broad hand‑tool portfolios remain powerful distribution partners and set the benchmark for product reliability and brand trust. Their scale supports investments in certification and channel programs, but they must avoid margin erosion in price‑sensitive segments.

- Professional / performance brands — firms focused on job‑site durability and professional features are driving product differentiation (reinforced bodies, wide blades, high‑visibility printing, reinforced hooks). These brands can leverage trade loyalty and spec‑based procurement to sustain premium pricing.

- Precision and specialist makers — companies with a heritage in measurement accuracy and ergonomic design command professional and survey segments where certification and fine tolerances matter most.

- High‑volume manufacturers — cost‑focused producers serve commodity channels and OEM demand; their advantage is scale and cost control, but they are vulnerable to raw‑material volatility and regulatory scrutiny.

Recent early‑2026 product activity underscores these dynamics: notable catalog updates and second‑generation product launches emphasize clip compatibility, hook coatings, and refined retraction systems. Independent head‑to‑head testing (early 2026) has amplified buyer attention on feature‑level differences — a trend that smart competitors will convert into marketing and spec wins.

Regulatory changes: a new compliance baseline

NIST’s 2026 Handbook updates have established a clearer, stricter tolerance regime for measuring devices used in commerce. For example, the accuracy requirement for a 1.82‑meter (6‑foot) tape used in buying and selling mandates a tight per‑tape tolerance — a rule that raises the bar for production quality control, in‑line testing, and certification documentation. The practical impact is threefold:

- Manufacturers must invest in measurement labs, calibration processes, and traceability programs to retain access to regulated procurement channels.

- Certifications will become purchase‑decision triggers in professional and commercial procurement — products lacking verifiable compliance risk contract exclusion.

- Compliance costs will disproportionately affect low‑margin producers, potentially accelerating consolidation or niche specialization.

Supply‑chain realities and raw‑material scenarios

Steel and fiberglass remain the primary input materials for tape measures. Price swings, trade policy shifts, and capacity constraints in these commodity markets are first‑order risk factors. Our scenario work shows that modest increases in steel pricing, without commensurate repricing discipline, can erode gross margins for mid‑market producers. Recommended mitigations include:

- Strategic hedging and longer‑term purchase agreements for key inputs.

- Selective vertical integration or preferred supplier partnerships to secure continuity and quality control.

- Near‑sourcing strategies to reduce transit lead times and tariff exposure where the economics support it.

Actionable moves for 2026 planning cycles

For executives preparing 2026 budgets and three‑year plans, prioritize initiatives that protect margin while capturing the growing premium segment:

- Compliance as a competitive moat: budget explicitly for NIST‑aligned QA capabilities and certification timelines — this is market access insurance for professional channels.

- Product portfolio rationalization: eliminate low‑return SKUs, concentrate R&D on blade readability, hook durability, casing ergonomics, and premium retraction mechanics that testing organizations now prize.

- Channel segmentation and pricing architecture: build differentiated offers for pros vs. DIY, with clear value communication around warranty, certification, and replacement cycles.

- Supplier resilience: implement dual‑sourcing for steel and fiberglass, and evaluate hedging or forward contracts for the largest spend buckets.

- M&A and partnerships: identify bolt‑on targets that add complementary product features, testing capabilities, or access to professional channels — mid‑market consolidation can be accretive on both revenue and margin.

- Innovation pipeline: explore digitization pathways (smart measuring aids, data capture integration) that extend the utility of tape measures into adjacent workflows without overcomplicating the core product promise.

What PW Consulting’s Tape Measures report delivers

This report is designed as a practical playbook for 2026 decision‑makers. Key deliverables include:

- Market sizing and a seven‑year forecast with high‑granularity demand scenarios (base, upside, downside) and sensitivity to raw‑material costs.

- Competitive benchmarking across product features, channel strength, certification credentials, and R&D focus.

- Product‑level matrices and model comparisons based on durability, accuracy, ergonomics, and job‑site suitability.

- Go‑to‑market strategies with channel maps, pricing frameworks, and trade promotion optimization guidance.

- Regulatory compliance checklist aligned to the latest NIST specifications and recommended test‑lab investments.

- Supply‑chain scenarios and procurement playbooks for steel and fiberglass risk mitigation.

- M&A target shortlist and a due‑diligence template tailored for both strategic acquirers and financial sponsors.

- Primary research appendices: interview transcripts with trade buyers, technical evaluations, and independent testing summaries.

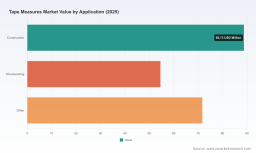

To preserve the competitive value of our work while inviting further engagement, the public summary intentionally omits granular regional and application‑level splits and detailed model‑level market shares. Those data tables and interactive dashboards are available in the full report.

How to use this intelligence in 90–180 days

- Use the compliance checklist to finalize capital requests for measurement labs and certification timelines (90 days).

- Implement a SKU rationalization pilot targeting 10–15% of slow‑turn inventory and reallocate R&D to two prioritized feature enhancements (120 days).

- Launch supplier negotiations for multi‑quarter steel/fiberglass agreements and evaluate one potential near‑shore supplier for a pilot production run (180 days).

In a market that grows predictably but tightens on technical and regulatory expectations, the winners in 2026 will be those who convert engineering precision into certified commercial value, and who align procurement and channel strategies to protect margin. PW Consulting’s Tape Measures Market report gives you the calibrated overview and the tactical tools to do exactly that.

Next steps

Access the full report to obtain the detailed regional and application splits, model‑level benchmarking, and the interactive forecast model that underpins these recommendations. For bespoke workshops, competitive deconstruction, or M&A due diligence tailored to your portfolio, contact PW Consulting — we will map these insights into an executable plan for 2026.

For detailed analysis of this topic, please visit the official page: Tape Measures Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com