@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting Forecasts Merchant Embedded Computing Market to Reach USD 344.8 Million by 2032, Growing at a 7.02% CAGR (2026–2032)

The Merchant Embedded Computing Market: Strategic Imperatives for 2026 — PW Consulting Release

PW Consulting today releases an executive briefing accompanying our full-market study, The Merchant Embedded Computing Market (base year 2025). As global commerce and industrial edge architectures converge, merchant embedded computing platforms — the small, rugged, and highly-integrable compute modules that power payment terminals, kiosks, industrial controllers, medical appliances, and mission-critical devices — are rapidly moving from commodity components to strategic enablers. This briefing outlines why our report is essential for boardroom decision-making in 2026, summarizes market momentum and structural dynamics, and explains how the report’s practical toolset de-risks vendor selection, product roadmaps, and regulatory planning. (Note: detailed segment-level tables and proprietary worksheets are intentionally withheld from this public summary; request full access via the report landing page.)

The Merchant Embedded Computing Market

Market snapshot: steady expansion, measurable runway

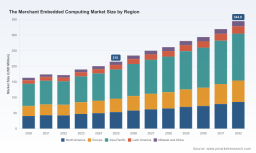

Using 2025 as the base year, PW Consulting’s analysis shows the merchant embedded computing market is on a sustained growth trajectory. In 2025 the market reached an estimated USD 215.0 Million (revenue unit: Million USD). Under the baseline scenario and with conservative assumptions around component pricing and supply recovery, we project the market to expand to roughly USD 234.6 Million in 2026 and to exceed USD 344.8 Million by 2032 — reflecting a compound annual growth rate (CAGR) of approximately 7.02% over the 2026–2032 forecast period. This pace reflects a mix of incremental replacement cycles, new deployments at the network edge, and a rising share of AI-enabled embedded systems.

The Merchant Embedded Computing Market

What is driving growth — and what is holding it back?

-

Demand drivers: The combination of digital payments expansion, factory and process automation, intelligent kiosks, and edge AI for predictive maintenance continues to create persistent demand for merchant-grade embedded computing platforms. OEMs and systems integrators increasingly prefer modular, COTS (commercial off-the-shelf) boards and systems that shorten time-to-market while supporting ruggedized deployments and extended lifecycle support.

The Merchant Embedded Computing Market -

Regulatory and certification pressures: The regulatory landscape is tightening in several jurisdictions. New requirements — including energy-efficiency and safety certification expectations tied to regional green initiatives and emerging AI regulatory frameworks — are shaping design priorities. For payments use cases, compliance with payment security standards such as PCI DSS remains a gating item for any solution that directly handles cardholder data.

-

Supply chain and cost pressures: The industry continues to feel the aftershocks of post-pandemic component constraints and upward pricing pressure on semiconductor components. Simultaneously, a shortage of embedded-systems skills in many SMEs is slowing integration cycles and increasing total cost of ownership for some projects.

-

Standards and interoperability gaps: A significant growth limiter remains the lack of consistent interoperability and standardization across merchant embedded platforms. This friction increases integration complexity for systems integrators and reduces the effective addressable market for vendors with narrowly focused stacks.

What PW Consulting’s report delivers to decision-makers

We designed this study to be a practical playbook for commercial and technical executives who must make 2026 investment decisions quickly and with confidence. Highlights of the report’s hands-on content include:

-

Proven vendor selection framework — a multi-criteria scoring model that weights performance, lifecycle support, compliance readiness, and supply-chain resilience to identify optimal partners for different risk profiles.

-

Total Cost of Ownership templates — configurable calculators that factor in procurement, integration, certification, maintenance, and planned hardware refreshes, enabling side-by-side comparisons across platform classes.

-

Regulatory compliance checklists — actionable remediations and evidence trails aligned to PCI DSS for payments integrations and to current regional safety and energy-efficiency expectations tied to AI governance and CE requirements.

-

Technology roadmaps — a matrix of processor, I/O, connectivity, and security trends that matter for the next 36–60 months, including recommended upgrade paths for fielded deployments to accommodate edge AI workloads.

-

Supply chain and sourcing playbook — scenario maps and risk mitigations for component shortages, alternate sourcing, and inventory strategies tailored to OEMs, ISVs, and integrators of different scale.

-

Market-entry and GTM playbooks — route-to-market templates that identify profitable adjacencies, strategic OEM partnerships, and channel models for scale without compromising operational security or certification timelines.

Competitive landscape — fragmented market, specialized leaders

The merchant embedded computing market remains structurally fragmented. Market concentration metrics point to a low level of dominance by a few players (CR3 ~24.6%; CR5 ~26.2%), which signals an open competitive environment where vertical specialization, certification capabilities, and ecosystem partnerships drive differentiation more than sheer scale.

Key vendors profiled in the report include established embedded and industrial computing specialists whose product and go-to-market approaches exemplify the range of strategies available to buyers:

-

Advantech Co., Ltd. (Taipei, Taiwan) — known for industrial-grade merchant embedded platforms and ruggedized systems used across digital payment and harsh-environment applications. In 2025 the company announced a new line of AI-enabled embedded systems that offer materially faster processing for automation use cases.

-

ADLINK Technology Inc. (Taipei, Taiwan) — positions strongly in edge compute modules optimized for industrial automation and real-time workloads. In late 2025 ADLINK launched modules targeting Edge AI systems that expand capabilities for inference at the network edge.

-

Kontron AG (Augsburg, Germany) — a provider of commercially hardened off-the-shelf solutions that target both merchant and industrial applications, with a focus on long-term availability and standards compliance.

-

Curtiss-Wright Corporation (Charlotte, NC, USA) — supplies rugged systems for mission-critical and payment environments where reliability and extended lifecycle support are non-negotiable.

-

Mercury Systems, Inc. (Chelmsford, MA, USA) — emphasizes high-performance boards and modules for defense and industrial integration projects where specialized security and processing are required.

-

Regional specialists — multiple Taiwan-based and other regional firms offer compact, fanless, and highly-integrable platforms tailored to payment and edge use cases; these vendors often win on customization, cost-effectiveness, and rapid OEM support cycles.

Recent product moves and their practical implications

-

ADLINK’s late-2025 release of i-MX95-based modules signals accelerated vendor competition around edge AI-capable compute bricks. For systems architects this means higher baseline processing at similar power and form-factor constraints — enabling richer local analytics but increasing demands on secure firmware management.

-

Advantech’s early-2025 announcement of AI-enabled embedded systems, with claimed performance improvements over prior generations, underscores an industry pivot: vendors are bundling compute performance and domain-specific middleware to shorten integration cycles. Buyers should evaluate whether such bundled approaches reduce integration risk or lock them into heavyweight upgrade paths.

Strategic recommendations for 2026 planning

For CEOs, CTOs, and procurement leaders preparing budgets and product roadmaps in 2026, PW Consulting’s study distills three immediate imperatives:

-

Prioritize certification and security as first-order design objectives. Certification delays and incomplete compliance scopes are among the most common reasons for go-to-market slippage in payments and regulated devices.

-

Design for modular upgradeability. Given the pace of change in edge AI and energy-efficiency expectations, architectures that allow field-level module swaps and secure firmware updates materially extend deployed lifecycles and reduce TCO.

-

Adopt an active sourcing strategy that blends Tier-1 suppliers with vetted regional specialists. Because the market is fragmented, suppliers offering niche capabilities may provide superior value if they meet compliance and long-term support criteria.

How to use this report in practice

The full PW Consulting report is organized to support executable decisions: an executive dashboard for quick board updates, an annex of supplier scorecards for procurement, and technical appendices with software and hardware integration checklists for engineering teams. It also includes scenario-based financial models and negotiation playbooks tailored to different procurement volumes and risk appetites.

Because this briefing follows a “trailer” approach — demonstrating the depth of our analysis while omitting proprietary segment-level tables and worksheets — organizations that require procurement-ready artifacts, vendor scorecards, or hands-on workshops to operationalize these insights should request the full report package and the associated consulting workshop from PW Consulting.

Next steps — who should read the full report

-

Board members and corporate strategists evaluating edge computing investments and product portfolio rationalization.

-

CTOs and chief architects planning embedded platform roadmaps for payment terminals, kiosks, medical devices, and industrial controls.

-

Procurement and supply-chain leaders seeking a defensible sourcing strategy for modules, boards, and integrated systems.

-

Investors and M&A teams assessing consolidations or carve-outs in a fragmented vendor landscape where strategic fit, certification capabilities, and channel reach drive valuation differentials.

Closing note

Merchant embedded computing is no longer a purely technical decision; it is a cross-functional strategic lever that affects compliance, go-to-market velocity, and long-term cost profiles. With a market that is expanding at a mid-single-digit CAGR and clear inflection points driven by edge AI, regulation, and evolving payment architectures, 2026 will be a pivotal year for organizations that act early. PW Consulting’s full-market study and actionable toolkits are designed to help leaders turn uncertainty into competitive advantage — contact our research team to obtain the complete report and tailored advisory options.

For detailed analysis of this topic, please visit the official page: The Merchant Embedded Computing Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com