@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting Forecasts Crude Tall Oil Derivatives Market to Expand at a 3.88% CAGR Through 2032

Crude Tall Oil Derivatives: Strategic Insights for 2026 Decision-Makers

Executive snapshot

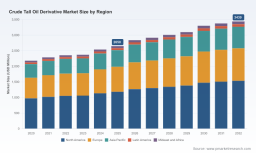

PW Consulting’s latest Crude Tall Oil (CTO) Derivative Market study (base year 2025; historical coverage 2020–2025; forecast period 2026–2032) delivers a pragmatic, decision-ready view of an evolving pine-chemicals landscape. Our modelling projects the global CTO-derived market to grow from approximately USD 2,650 Million in 2025 to roughly USD 3,439 Million by 2032, corresponding to a 3.88% compound annual growth rate across the 2026–2032 horizon. Market concentration remains meaningful but not prohibitive (CR3 ≈ 48%; CR5 ≈ 52%), creating both competitive pressure and opportunity for mid-sized challengers.

Crude Tall Oil Derivative Market

Why this matters for 2026 strategy

- Regulatory and feedstock shifts are altering cost dynamics and demand mix in real time. Executives who translate scenario-ready intelligence into contract and capital decisions in 2026 will materially influence their margin trajectories through the early 2030s.

- Price volatility and recent supply-side restructurings are amplifying short-term commercial leverage for producers with flexible refining capacity and secure raw-material agreements.

- Investors and corporate development teams should treat CTO derivatives both as a chemicals growth play and a strategic feedstock hedge against tightening biodiesel and renewable diesel markets—especially where policy interventions accelerate bioblend mandates.

Key demand and supply dynamics shaping 2026 choices

The report integrates macro drivers that will be particularly active in 2026. Policy initiatives—most notably proposed increases to U.S. biodiesel mandates and tightening EU trade remedies—are lifting the strategic importance of CTO as a non-food, lignocellulosic feedstock that can bridge biofuel and specialty-chemicals demand. At the same time, trade measures and lumber tariffs in North America have reduced pulp throughput in some jurisdictions, creating episodic supply tightness that will shape short- and medium-term pricing.

Crude Tall Oil Derivative Market

Operational shifts at mills (including changes in biomass-burning practices under evolving renewable-energy rules) are increasing the yield efficiency of CTO in some regions, while refinery rationalizations and asset sales are concentrating processing capability in others. These dynamics are producing two simultaneous phenomena: higher headline demand for CTO-derived biofuels and specialty chemicals, and increased price sensitivity where refining capacity is constrained.

Crude Tall Oil Derivative Market

Recent market events with direct commercial implications

- Kraton Corporation announced stepped price increases across TOFA and CTO-refinery portfolios in late 2025 and early 2026—moves that reflect both feedstock tightening and opportunistic pricing power in EMEA and globally. Commercial teams should anticipate pass-through dynamics and re-price-offtake terms accordingly.

- Ingevity’s divestment of a North Charleston CTO refinery (completed in early 2026) illustrates active portfolio reallocation in the industry: owners are either consolidating upstream pulp-linked supply or exiting non-core processing assets, creating M&A and contract renegotiation windows for buyers.

- Policy signals—such as proposed biodiesel mandate changes and EU anti-dumping duties—are materially reconfiguring the competitive positioning of CTO versus alternative biofeedstocks. Buyers and refiners must incorporate these regulatory sensitivities into 2026 procurement and capital planning.

Competitive landscape — tactical implications

The CTO derivatives ecosystem includes integrated pulp producers, stand-alone refiners, and specialty-chemicals firms. The report’s competitive benchmarking covers leading global players and emerging regional processors. Key industry participants profiled include:

- Kraton Corporation (Houston, Texas, United States) — a significant refiner and supplier of TOFA and pine-based specialties; recent pricing actions signal market influence and a focus on margin recovery. ( https://kraton.com)

- UPM-Kymmene Oyj (Helsinki, Finland) — supplies CTO from pulping operations and leverages integration to feed renewable-fuel and chemical value chains. ( https://www.upm.com)

- Stora Enso Oyj (Helsinki, Finland) — a Nordic, pulp-integrated supplier with established feedstock flows into pine-chemical derivatives. ( https://www.storaenso.com)

- Ilim Group JSC (Moscow, Russia) — an important mill-supplier and refiner whose operational footprint can influence regional availability. ( https://www.ilimgroup.com)

- Forchem Oyj, Fintoil Oy, Harima Chemicals Group, SunPine AB, Eastman Chemical Company — specialist refiners and downstream integrators whose differing business models (distillation, biorefining, renewable-diesel production, chemical conversion) create alternative strategic pathways for buyers and partners. (See company sites for corporate disclosures.)

These profiles are paired in the full report with transaction histories, balance-sheet exposures to feedstock price, and scenario-based profitability ladders—items that are deliberately summarized here to preserve proprietary model outputs.

What our report delivers (practical, operational content)

PW Consulting designed this study as a hands-on playbook for 2026. Key deliverables include:

- Forward-looking supply-demand modelling (2026–2032) that isolates the impacts of biofuel mandates, trade remedies, and pulp-mill operating changes on CTO availability and price pressure.

- Scenario workbooks (baseline, accelerated-biofuel, supply-shock, and regulatory-tightening), with actionable trigger points for contract re-pricing, capacity ramp or idling, and contingency sourcing.

- Competitive scorecards and M&A screens: refined target lists built from operating-scale, feedstock security, and integration-readiness metrics that prioritize near-term bolt-on and platform-scale opportunities.

- Commercial playbooks: negotiation checklists, indexation approaches for offtake contracts (including suggested hedging instruments), and short-term procurement levers to preserve margin in periods of refinery consolidation or feedstock scarcity.

- Capex decision frameworks that quantify payback timelines for debottlenecking, distillation upgrades, and downstream functionalization (rosin-resin conversions, TOFA fractionation), accounting for varying policy outcomes.

- Sustainability and compliance modules mapping RED III, potential EPA mandate changes, and other regulatory levers to product eligibility for renewable fuel credits and green-chemicals certification.

Strategic recommendations for 2026 (actionable priorities)

- For refiners: prioritize flexible fractionation and distillation capacity that allows rapid SKU shifting between TOFA, rosin derivatives, and pitch—this flexibility is the most valuable hedge against near-term price shocks and evolving product demand from biofuels.

- For integrated pulp producers: monetize feedstock via differentiated contracts that extract premium for sustainability-compliant CTO and consider joint ventures with refiners to capture downstream margin.

- For chemical companies and end-users (coatings, adhesives, surfactants): secure multi-year offtakes with indexation clauses that protect against input spikes, and evaluate backward integration where logistics or feedstock access is a competitive bottleneck.

- For private equity and corporate M&A teams: target mid-tier refiners and regional processors that offer rapid scale-up potential through bolt-on distillation and functionalization assets; value creation is concentrated in converting feedstock access into specialty-chemicals capabilities.

- All players should embed two 2026-ready scenario triggers into board-level risk frameworks: (1) a regulatory acceleration trigger (e.g., higher-than-expected bioblend mandates) that favors supply-secure producers and converts TOFA into fuel feedstock at scale; and (2) a supply-contraction trigger (e.g., mill outages, tariff-driven pulp reductions) that creates short windows for price recovery—both require pre-specified contract and capex responses.

Why PW Consulting’s analysis is decisive for 2026

Our approach combines granular mill-to-refinery supply mapping, policy-sensitivity overlays, and proprietary price-transmission modelling calibrated to late-2025 and early-2026 market events. The report synthesizes public disclosures, transaction evidence (including recent asset sales and company price actions), and bottom-up yield modelling to convert headline trends into commercial actions. We intentionally limit detailed segmentation in public summaries to preserve the tactical value of the full data suite; companies that integrate these datasets into 2026 planning will have a measurable edge in contract negotiations, asset allocation, and portfolio optimization.

Next steps — how to use the report

- Procurement and commercial teams: adopt the report’s negotiation templates and index-protection approaches in Q1–Q2 2026 renegotiations.

- Strategy and corporate development: use the M&A screens and scorecards to prioritize targets and prepare pre-emptive bid dossiers for likely divestments and distressed assets.

- Operations and capex planners: run the scenario workbooks against existing project pipelines to determine deferment or acceleration decisions tied to policy milestones.

Accessing the full intelligence

This press release is a strategic preview. The full PW Consulting Crude Tall Oil Derivative Market report contains the detailed regional, product and application splits, downloadable datasets (USD Million), interactive scenario models, and playbooks referenced above. These detailed tables and model outputs are intentionally withheld here to ensure decision advantage for report subscribers.

To obtain the complete report, interactive tools, and client-only briefing sessions (including a 90-minute, tailored strategy workshop for leadership teams), please visit our report page or contact PW Consulting’s industry desk. Equip your 2026 decision-making with the modelling and commercial playbooks that convert market complexity into competitive advantage.

For detailed analysis of this topic, please visit the official page: Crude Tall Oil Derivative Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com