@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting: Aircraft Piston Engines Market Poised to Reach USD 7.15 Billion by 2032, Growing at 5.2% CAGR (2026–2032)

Aircraft Piston Engines Market — Strategic Outlook for 2026: A PW Consulting Brief

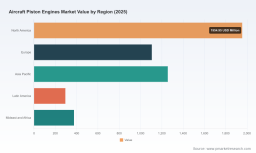

PW Consulting’s latest market study on Aircraft Piston Engines frames a decisive window for executive action in 2026. Our base-year sizing places the global market at USD 4,988.5 Million (2025), after a recovery from the 2020 trough, and our forecast modeling—built on a range of macro and micro drivers—projects growth through 2032 at a 5.2% CAGR to a projected market value above USD 7.1 Billion by the end of the forecast horizon. The market remains structurally fragmented (CR3 ~24.6%; CR5 ~26.2%), creating both opportunity and risk for incumbents and new entrants. This brief highlights the report’s strategic value and the specific decision levers that matter for 2026, while reserving the detailed subsegment tables and proprietary models for report subscribers.

Aircraft Piston Engines Market

Why PW Consulting’s 2026 Perspective Matters

- Timing: Multiple certification events and product launches across 2024–2026 are accelerating structural change in powerplant choice and fuel strategy. These inflection points affect product roadmaps, supply commitments and certification calendars that must be locked in during 2026.

- Scale-up pressures: Manufacturers face a near-term trade-off between scaling production to capture demand and preserving balance-sheet resilience. Our report quantifies the cost and lead-time implications of those paths and translates them into executable options for 2026.

- Fragmentation-driven consolidation: Low top-three/top-five concentration signals an open field for M&A roll-ups, bolt-on acquisitions and carve-outs—opportunities that investors and strategics can model now to capture early-mover advantages.

- Fuel and platform transitions: The emergence of jet-fuel-burning piston engines and FADEC integration creates differentiated routes-to-market—affecting aftermarket dynamics, training, and type-specific service networks.

What the Report Delivers (Practical, Transaction-Ready Content)

- Robust market sizing and trajectory (historical 2020–2025; base year 2025; forecast 2026–2032) with transparent methodology and sensitivity scenarios.

- Decision-grade scenario models for product development, certification timelines and go-to-market sequencing (including upside/downside cases calibrated to certification and delivery risks).

- Supplier and OEM scorecards highlighting manufacturing scale, certification maturity, and aftermarket depth—presented as prioritized action lists rather than raw tables.

- Investment and M&A playbooks: valuation yardsticks, earn‑out structures tailored to the sector’s certification risk, and 100‑day integration checklists for acquisition targets.

- Operational benchmarks and CAPEX/OPEX templates for greenfield engine production, overhaul facilities and FADEC/electronics integration.

- Regulatory pathways and test-sequence playbooks—mapping FAA and EASA milestones to commercial go/no-go decision gates.

Recent Industry Signals That Should Shape 2026 Strategy

- Certification momentum for heavy‑fuel (Jet‑A) piston engines: Notable approvals and type certifications in 2024–2026 are validating the technical viability and commercial appeal of heavy‑fuel piston powerplants for certain rotorcraft and fixed-wing segments.

- Program launches tying OEM airframes to new engine platforms have moved from announcement to flight-testing phases—creating early adopters and supply commitments that shift competitive positioning within months.

- End-market demand for piston‑powered aircraft has shown renewed strength—GAMA reported a 4.2% increase in piston airplane deliveries in 2024—supporting a sustained aftermarket recovery and new engine orders.

Competitive Positioning: Strategic Takeaways on Core Players

Our competitive analysis synthesizes public disclosures, certification milestones and product portfolios to evaluate where each player is positioned strategically for 2026 decisions.

Aircraft Piston Engines Market

- Lycoming Engines (Williamsport, PA) — Deep installed base and legacy strength across four- to eight‑cylinder offerings provide defensive advantages in replacement parts and overhaul. Strategic focus in 2026 should be on monetizing installed-base services, modernizing engine variants with digital controls, and selectively partnering where Jet‑A adoption could cannibalize legacy avgas demand.

- Continental Aerospace Technologies (Mobile, AL) — Technological pivot evident in Jet‑A and FADEC developments has positioned Continental to capture rotorcraft and special-mission opportunities; EASA approvals for Jet‑A piston platforms underline cross-jurisdiction ambitions. For 2026, Continental’s playbook should emphasize supply partnerships and aftermarket certification support to accelerate adoption.

- BRP‑Rotax (Austria) — Clear leadership in light sport, ultralight and training segments, with product roadmaps tuned to lightweight, efficient powerplants. Strategic questions for 2026 involve leveraging these strengths into adjacent segments via certification investments or selective co-development agreements.

- DeltaHawk Engines (Racine, WI) — Represents the disruptive end of the spectrum with FAA‑certified, jet‑fuel-burning piston engines gaining in-program validation. DeltaHawk’s early wins create a strategic imperative for incumbents to respond—either by competing directly, partnering for integration, or differentiating around service ecosystems.

Case Signals: Product Launches and Certifications to Watch

- OEM engine-airframe pairings moving into flight testing and certification (announced and underway in 2024–2026) create discrete adoption windows. Commercial and procurement teams must re-evaluate type-approval contingencies and service-bulletin pipelines in 2026.

- Regulatory milestones—FAA type certifications and EASA approvals—are acting as market accelerants. Certification timelines should be treated as critical path items for capital allocation and supplier contracting.

Actionable Recommendations for 2026

- Engine OEMs: Prioritize dual‑fuel and FADEC-enabled variants where certification timelines are favorable; allocate development budgets to high-margin aftermarket services and digital diagnostics. Use the report’s scenario outputs to time capacity increases to match certified ramp-ups.

- MROs and Service Networks: Invest in training programs and tooling ahead of expected certification-driven fleet conversions. Position service centres as preferred partners for engine swaps by demonstrating turn‑key support (logistics, paperwork, and training bundles).

- Investors and PE: Target roll‑up plays in a fragmented competitive landscape—look for assets with service revenue streams and short certification tails. Our valuation templates and integration checklists de‑risk near-term acquisitions.

- Airframe OEMs: Negotiate long‑lead supplier agreements and certification support clauses into engine supply contracts; consider equity or strategic partnerships with emerging heavy‑fuel engine suppliers to secure differentiated propulsion options.

- Policy and Regulator Engagement: Engage early with certification authorities to clarify test protocols and acceptance criteria for heavy‑fuel piston engines—these interactions materially influence program risk and timing.

Methodology and Confidence Calibration

The report’s base-year and historical analysis covers 2020–2025, with a 2025 base year and a forecast window of 2026–2032. Revenue figures are expressed in USD Million. Our forecasts combine bottom‑up OEM program analyses, aftermarket demand modeling, and macro demand drivers, and include probabilistic scenario overlays to capture certification, supply-chain, and macroeconomic variability. Where sensitivity is high—particularly around type‑approval timelines and fuel‑policy shifts—we provide high/medium/low cases to support binary investment decisions.

Aircraft Piston Engines Market

How to Use This Brief in Your 2026 Planning Cycle

- Embed the scenario outputs into capital planning and supplier contracting to avoid over-commitment ahead of certification milestones.

- Use the M&A playbooks to evaluate roll‑up targets and structure offers that price in certification risk and integration cost.

- Leverage the supplier scorecards and operational benchmarks to renegotiate lead-times and reduce single-point-of-failure exposure.

- Adopt the regulatory playbooks to shorten certification cycles by proactively aligning test programs and evidence packages with FAA/EASA expectations.

Next Steps

PW Consulting’s full Aircraft Piston Engines Market report contains the comprehensive subsegment tables, regional breakdowns, company-level revenue pockets, downloadable financial models and supplier scorecards that underpin the strategic guidance summarized here. For commercial teams, product executives, M&A leads and investors preparing 2026 budgets and roadmaps, the report converts market signals into executable decisions—and shows precisely where to allocate capital, people and time to capture the next wave of value in piston propulsion.

To access the full dataset, scenario models, and the step‑by‑step playbooks referenced in this brief, please consult the PW Consulting report page or contact your PW Consulting engagement lead.

For detailed analysis of this topic, please visit the official page: Aircraft Piston Engines Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com