@pmarketresearch

- Followers 0

- Following 0

- Updates 57

PW Consulting: Wire Marking Labels Market to Rise from USD 215.0M in 2025 to USD 302.14M by 2032 at 5.01% CAGR

Wire Marking Labels Market 2026: Strategic Imperatives from PW Consulting’s Market Intelligence

Executive summary

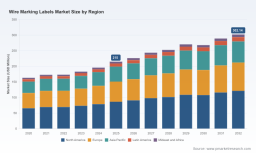

As enterprises recalibrate supply chains and product strategies for 2026, the wire marking labels market is emerging as a quietly resilient node within industrial identification and cable management ecosystems. PW Consulting’s new market research — with base year 2025 and a forecast window covering 2026–2032 — shows a market that has expanded from roughly USD 163 million in 2020 to USD 215 million by 2025 and is projected to continue growing at a compound annual growth rate (CAGR) of 5.01% through the forecast period. Our analysis positions the market at approximately USD 226 million in 2026 and anticipates continued expansion toward a multi-hundred-million-dollar industry by 2032.

Wire Marking Labels Market

Why this matters for 2026 decision-makers

-

Margin and procurement planning: modest but steady growth and a moderate concentration profile (CR3 ≈ 52%; CR5 ≈ 64%) create a competitive environment where scale matters for cost-out, but focused differentiation can preserve premium margins.

Wire Marking Labels Market -

Product roadmaps and sustainability: regulators and procurement specifications increasingly demand recycled-content claims and validated environmental credentials, altering material sourcing and product specifications.

Wire Marking Labels Market -

Channel and service offerings: as data-center, telecommunications, industrial automation and traditional electrical segments evolve, manufacturers and distributors must choose between expanding breadth (catalog and global footprint) and investing in value-added services (printing, kitting, lifecycle traceability).

Market trajectory: context and near-term inflection points

Between 2020 and 2025 the market registered steady expansion, reflecting resilient demand across electrical and communications infrastructure, combined with growing replacement and retrofit activity. Our 2026 projection places the market at about USD 226 million; by 2032 we forecast sustained growth into the low hundreds of millions (reflecting overall sector maturation and pockets of technology-driven premiumization). The 5.01% CAGR included in our model is conservative relative to many adjacent industrial identification categories — it reflects structural demand stability alongside episodic volatility in raw material prices and regulatory shifts.

Key strategic implications

-

Prioritize supply-chain agility over lowest-cost sourcing. Raw-material volatility (notably plastic resin indices) and trade-policy dynamics make single-source strategies risky. Firms that implemented diversified sourcing and strategic inventory buffers in 2023–25 outperformed peers on fill rates in early 2026.

-

Invest in validated sustainability claims. Extended Producer Responsibility (EPR) frameworks and recycled-content standards (including third-party validations) are now procurement gatekeepers for large OEMs and infrastructure projects. Early investments in mass-balance certification and post-consumer content integration materially reduce commercial friction.

-

Service differentiation drives margin. Companies offering integrated identification systems (label materials, print/hardware, software for asset tagging and lifecycle management) can capture higher wallet share from enterprise customers compared with pure consumables vendors.

-

Data-driven commercial segmentation is essential. With a moderately concentrated market structure, precise account-level strategy (targeting high-value verticals and use-cases) produces substantially higher ROI than geographic expansion without service differentiation.

Competitive landscape: what incumbents are doing

The market combines global industrial players, specialty labeling providers, and regional distributors. Our coverage focuses on strategic positioning and recent maneuvers by leading vendors who shape market dynamics.

-

HellermannTyton — A leader with deep product breadth across industrial cable labels, printable shrinkable sleeves and identification systems. Recent investments include a new manufacturing facility in Chennai (inaugurated late 2025) and a Product Catalogue 2026 emphasizing smart cable management. These moves demonstrate a two-track strategy: localized production to address trade/tariff sensitivity and a catalog-driven push toward integrated solutions.

-

Brady Corporation — Brady’s acquisition of Mecco Partners in 2025 strengthened its systems capabilities for industrial marking and on-site identification. This builds on Brady’s longstanding focus on durable, print-enabled labelling systems for complex installations, improving its ability to offer bundled hardware-plus-consumable solutions.

-

3M — The company’s strength remains in premium, high-durability substrates and certifications for harsh environments. 3M’s value proposition is reliability and longevity, which is particularly compelling for mission-critical infrastructure with high life-cycle cost sensitivity.

-

Lapp Group and Panduit — Both firms emphasize industrial and data-center applications respectively, with product portfolios and channel strategies targeting automation and communications infrastructure. Panduit’s positioning in data centers and Lapp’s deep industrial integrations illustrate the vertical specialization that is increasingly profitable.

-

Seton and Silver Fox — These firms exemplify differentiated regional and service-focused plays, maintaining relevance through customer intimacy, fast delivery, and customized identification solutions for maintenance and safety applications.

Recent market actions to watch

-

Manufacturing footprint expansion into lower-cost and tariff-exempt jurisdictions (example: HellermannTyton’s Chennai facility) — a clear response to Buy-America-style provisions and tariffs.

-

M&A to acquire systems capabilities (example: Brady/Mecco) — consolidating hardware + software + consumable value chains to lock in enterprise accounts.

-

Product innovation: UV inkjet terminal markers and other next-generation offerings are pushing digital printing into identification workflows, shortening lead times for customized orders and enabling high-mix, low-volume profitability strategies.

Regulatory and raw-material environment: strategic considerations

Regulatory shifts and commodity dynamics are now first-order concerns for 2026 planning:

-

Extended Producer Responsibility and recycled-content mandates require clear supply-chain traceability. Compliance often demands third-party validation (for example, programs that define recycled content mass-balance and product-level claims), and failing to address this can block procurement opportunities with large enterprise and public-sector buyers.

-

Recycled-content standards (including third-party certifications requiring minimum post-consumer/pre-consumer thresholds) are not only compliance metrics but also market signals. They influence raw-material sourcing, production processes, and price realization.

-

Plastic resin price volatility, tracked by indices such as the producer price index, drives short-cycle margin risk. Pricing architectures (index-linked contracts, hedging, multi-tier pass-throughs) are now common tactical responses.

-

Trade policy and procurement rules (tariffs, Buy-America) materially affect localization and inventory strategies. Firms with flexible manufacturing footprints secure competitive advantage in large infrastructure tenders.

What PW Consulting’s report delivers (operational, not just academic)

Beyond headline market sizing and macro forecasts, our report is designed as an executable playbook for corporate leaders, product managers, and procurement chiefs. Key deliverables include:

-

Scenario-based demand models and sensitivity analyses that quantify revenue and margin impact across plausible raw-material price and regulatory scenarios for 2026–2032.

-

Go-to-market decision frameworks that align portfolio choices (consumables vs. integrated systems), distribution models (direct vs. distributor), and pricing strategies to customer lifetime value across verticals.

-

CapEx and footprint planning guidance. We provide decision heuristics for capacity allocation, near-shoring, and contract manufacturing based on total-cost-of-delivery and regulatory constraints.

-

M&A and partnership playbooks with value-capture estimates for tuck-ins vs. platform transactions — tailored to acquiring technology (printing/digitalization), materials capabilities, or regional reach.

-

Commercial templates: RFP language for sustainability compliance, supplier scorecards, and SKU rationalization matrices to reduce working capital and improve service levels.

How clients are using the intelligence

-

Strategic sourcing teams are using our index-linked pricing simulations to renegotiate long‑term resin contracts and to design pass-through clauses that protect margins without losing bids.

-

Product teams leverage our innovation scans to prioritize investments in printable sleeves and smart-label integration that yield the fastest route to premium positioning in data centers and automation projects.

-

Commercial leadership adopts our customer-segmentation playbook to reallocate sales resources toward high-LTV accounts and to build managed-service propositions that lock in recurring revenue.

Conclusion and next steps

The wire marking labels market in 2026 is a classic example of a mature industrial category that rewards disciplined operational excellence and selective innovation. Our market sizing — anchored in a 2025 base of USD 215 million and a forward-looking CAGR of 5.01% — demonstrates steady, actionable growth rather than speculative hypergrowth. For corporates preparing budgets, R&D roadmaps, or M&A pipelines in 2026, the choice is between tactical cost management and strategic repositioning toward services, sustainability, and digitalization.

PW Consulting’s full Wire Marking Labels Market report provides the granular datasets, scenario models, and supplier-level intelligence necessary to convert insight into 2026 action. Core subsegment allocations and full company-level financial detail are available exclusively in the full report; contact our research desk or visit the report page to access the complete dataset and tailored advisory options.

For detailed analysis of this topic, please visit the official page: Wire Marking Labels Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com